UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_________________________________________________

FORM 10-K

(Mark One)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended June 30, 2020

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission file number 1-11692

_________________________________________________

Ethan Allen Interiors Inc.

(Exact name of registrant as specified in its charter)

|

Delaware

|

|

06-1275288

|

|

(State or other jurisdiction of incorporation or organization)

|

|

(I.R.S. Employer Identification No.)

|

|

25 Lake Avenue Ext., Danbury, Connecticut

|

|

06811-5286

|

|

(Address of principal executive offices)

|

|

(Zip Code)

|

(203) 743-8000

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| |

Common stock $0.01 par value

|

|

ETH

|

|

New York Stock Exchange

|

|

| |

(Title of each class)

|

|

(Trading symbol)

|

|

(Name of exchange on which registered)

|

|

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☐ Yes ☒ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ☐ Yes ☒ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

| |

Large accelerated filer

|

☐ |

Accelerated filer

|

☒ |

| |

Non-accelerated filer

|

☐ |

Smaller reporting company

|

☐ |

| |

Emerging growth company

|

☐ |

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ☐ Yes ☒ No

The aggregate market value of the voting and non-voting common stock held by non-affiliates of the registrant on December 31, 2019, the last business day of the registrant’s most recently completed second fiscal quarter, was approximately $443,379,667. The number of shares outstanding of the registrant’s common stock, $0.01 par value, as of August 20, 2020 was 25,053,082.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement to be filed with the Securities and Exchange Commission pursuant to Regulation 14A for its 2020 Annual Meeting of Stockholders to be held as of November 12, 2020 are incorporated by reference into Part III of this Annual Report on Form 10-K where indicated. Such proxy statement will be filed with the Securities and Exchange Commission within 120 days of the registrant’s fiscal year ended June 30, 2020.

ETHAN ALLEN INTERIORS INC. AND SUBSIDIARIES

TABLE OF CONTENTS

| PART I |

|

|

| |

|

|

| Item 1. |

Business |

5 |

| |

|

|

| Item 1A. |

Risk Factors |

14 |

| |

|

|

| Item 1B. |

Unresolved Staff Comments |

22 |

| |

|

|

| Item 2. |

Properties |

22 |

| |

|

|

| Item 3. |

Legal Proceedings |

23 |

| |

|

|

| Item 4. |

Mine Safety Disclosures |

23 |

| |

|

|

| PART II |

|

|

| |

|

|

| Item 5. |

Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

24 |

| |

|

|

| Item 6. |

Selected Financial Data |

26 |

| |

|

|

| Item 7. |

Management's Discussion and Analysis of Financial Condition and Results of Operations |

27 |

| |

|

|

| Item 7A. |

Quantitative and Qualitative Disclosures About Market Risk |

43 |

| |

|

|

| Item 8. |

Financial Statements and Supplementary Data |

44 |

| |

|

|

| Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

80 |

| |

|

|

| Item 9A. |

Controls and Procedures |

80 |

| |

|

|

| Item 9B. |

Other Information |

80 |

| |

|

|

| PART III |

|

|

| |

|

|

| Item 10. |

Directors, Executive Officers and Corporate Governance |

81 |

| |

|

|

| Item 11. |

Executive Compensation |

81 |

| |

|

|

| Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

81 |

| |

|

|

| Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

82 |

| |

|

|

| Item 14. |

Principal Accountant Fees and Services |

82 |

| |

|

|

| PART IV |

|

|

| |

|

|

| Item 15. |

Exhibits and Financial Statement Schedules |

83 |

| |

|

|

| Item 16. |

Form 10-K Summary |

86 |

| |

|

|

| SIGNATURES |

|

87 |

ETHAN ALLEN INTERIORS INC. AND SUBSIDIARIES

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS (SAFE-HARBOR)

This Annual Report on Form 10-K contains certain statements which may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Generally, forward-looking statements give current expectations and projections relating to financial condition, results of operations, plans, objectives, future performance and business. A reader can identify forward-looking statements by the fact that they do not relate strictly to historical or current facts. These statements may include words such as “anticipate,” “estimate,” “expect,” “project,” “plan,” “intend,” “believe,” “continue,” “may,” “will,” “short-term,” “target,” “outlook,” “forecast,” “future,” “strategy,” “opportunity,” “would,” “guidance,” “non-recurring,” “one-time,” “unusual,” “should,” “likely,” “COVID-19 impact,” and other words and terms of similar meaning in connection with any discussion of the timing or nature of future operating or financial performance or other events.

Forward-looking statements are subject to risks and uncertainties that may cause actual results to differ materially from those that are expected. Ethan Allen Interiors Inc. and its subsidiaries (the “Company”) derive many of its forward-looking statements from operating budgets and forecasts, which are based upon many detailed assumptions. While the Company believes that its assumptions are reasonable, it cautions that it is very difficult to predict the impact of known factors and it is impossible for the Company to anticipate all factors that could affect actual results and matters that are identified as “short term,” “non-recurring,” “unusual,” “one-time,” or other words and terms of similar meaning may in fact recur in one or more future financial reporting periods. Important factors that could cause actual results to differ materially from the Company’s expectations, or cautionary statements, are disclosed in Item 1A, Risk Factors, Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operations, and elsewhere in this Annual Report Form 10-K. All forward-looking statements attributable to the Company, or persons acting on its behalf, are expressly qualified in their entirety by these cautionary statements, as well as other cautionary statements. A reader should evaluate all forward-looking statements made in this Annual Report on Form 10-K in the context of these risks and uncertainties. Given the risks and uncertainties surrounding forward-looking statements, you should not place undue reliance on these statements. Many of these factors are beyond our ability to control or predict.

The forward-looking statements included in this Annual Report on Form 10-K are made only as of the date hereof. The Company undertakes no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise, except as otherwise required by law.

ETHAN ALLEN INTERIORS INC. AND SUBSIDIARIES

PART I

ITEM 1. BUSINESS

Overview

Founded in 1932 and incorporated in Delaware in 1989, Ethan Allen Interiors Inc., through its wholly-owned subsidiary, Ethan Allen Global, Inc., and Ethan Allen Global, Inc.’s subsidiaries (collectively, “we,” “us,” “our,” “Ethan Allen” or the “Company”), is a leading interior design company, manufacturer and retailer in the home furnishings marketplace. Today we are a global luxury international home fashion brand that is vertically integrated from design through delivery, which affords our clientele a value proposition of style, quality and price. We provide complimentary interior design service to our clients and sell a full range of furniture products and decorative accents through a retail network of approximately 300 design centers in the United States and abroad as well as online at ethanallen.com. The design centers represent a mix of independent licensees and Company-owned and operated locations. Our Company operates retail design centers located in the United States and Canada. The independently operated design centers are located in the United States, Asia, the Middle East and Europe. We also own and operate nine manufacturing facilities, including six manufacturing plants in the United States, two manufacturing plants in Mexico and one manufacturing plant in Honduras. Approximately 75% of our products are manufactured or assembled in these North American facilities.

Business Strategy

Our strategy has been to position Ethan Allen as a preferred brand offering complimentary design service together with products of superior style, quality and value to provide customers with a comprehensive, one-stop shopping solution for their home furnishing and interior design needs. In carrying out our strategy, we continue to expand our reach to a broader consumer base through a diverse selection of attractively priced products, designed to complement one another, reflecting current fashion trends in home decorating. We continuously monitor changes in home fashion trends through attendance at international industry events and fashion shows, internal market research, and regular communication with our retailers and design center design consultants who provide valuable input on consumer trends. We believe that the observations and input gathered enable us to incorporate appropriate style details into our products to react quickly to changing customer tastes. We are receiving strong customer interest in our recently introduced products including Lucy, a mid-century modern inspired upholstery collection and Farmhouse, a country cottage inspired furniture collection.

Our strong network of North American interior design consultants continues to create design solutions that best satisfy our customers’ needs. We believe changes in consumer spending and new habits being formed as a result of social distancing and sheltering in place brought about by the COVID-19 pandemic will create opportunities for our brand. Now more than ever, home is a haven, and we are here to help the customer reimagine their homes. We continue to generate business through our retail design center network and by interacting virtually with our customers through ethanallen.com. Our design consultants engage with customers working safely in our design centers and remotely utilizing technology, including the Ethan Allen inHome augmented reality app, the 3D room planner tool, Live Chat on ethanallen.com, Skype and FaceTime.

At Ethan Allen, our internet strategy is to generate business by combining technology with excellent personal service. Though our customers have the opportunity to buy our products online, we take the process further. With so much of our product customizable, we encourage our website customers to get personal help from our interior design professionals either in person or by chatting online with one of our qualified design consultants. This complimentary direct contact with one of our knowledgeable interior design consultants, whether remotely or in-person, creates a competitive advantage through our excellent personal service. This enhances the online experience and regularly leads to internet customers becoming customers of our network of interior design centers. In the past three months, we have seen our internet business double as we have increased our use of technology and the related customer experience.

We plan to further invest in our digital footprint, including our website, in order to enhance our customer experience. We are also continually improving our customers’ journey from the time they land on our website to the delivery of their purchase through our white glove home delivery service. We view the combination of online traffic and design center traffic in a holistic fashion whereby our customer generally experiences our brand on our website before visiting a design center in person. Our online traffic continues to increase each year and our marketing teams remain focused on enhancing our digital outreach strategies to further drive more traffic and keep our brand relevant in today’s social media oriented world.

ETHAN ALLEN INTERIORS INC. AND SUBSIDIARIES

Developments Regarding, and Actions Taken in Response to, COVID-19

On March 11, 2020, the World Health Organization declared the COVID-19 outbreak to be a global pandemic. In response to this declaration and the rapid ongoing spread of COVID-19 within the United States and around the world, federal, state and local governments have imposed varying degrees of restrictions on social and commercial activity to promote social distancing in an effort to slow the spread of the virus. Such measures included quarantines, shelter-in-place orders and directives, restrictions on travel, and closures of non-essential businesses, which included many sectors within retail commerce. In response to these requirements and for the protection of our employees and customers, we implemented certain business continuity plans to ensure the ongoing availability of our services, while prioritizing health and safety measures, including temporarily closing of our design centers and most of our manufacturing plants, implementing enhanced cleaning and hygiene protocols as recommended by the Centers for Disease Control and Prevention (“CDC”), and implementing remote work policies, where possible.

The Company began to experience the initial impact of COVID-19 on customer demand in the second half of February 2020 and the decreased demand continued to persist into our fiscal 2020 fourth quarter. As a result, the Company implemented a number of mitigating safety and cost-saving measures.

On March 19, 2020, we announced that our Company-owned retail design centers in North America were temporarily closed or remained open by appointment only, in response to the COVID-19 health crisis. We continued to serve our clients by appointment in our physical locations or virtually. For the well-being of our associates, we also provided them the ability to work from home during this national health crisis, where possible.

On March 23, 2020, we borrowed an aggregate principal amount of $80 million under our existing revolving credit facility. Prior to such borrowing, there were no borrowings outstanding under the credit facility. On March 30, 2020, we borrowed an additional $20 million under the credit facility. We subsequently repaid $50 million of our borrowings in June 2020. The outstanding borrowings bear interest at a rate equal to the one-month LIBOR rate plus a spread using a debt leverage pricing grid. We may repay amounts borrowed at any time without penalty. The Company, while currently having available cash on its balance sheet and no outstanding debt, elected to draw on the credit facility to increase its cash position as a precautionary measure and to maximize financial flexibility in light of the uncertainty surrounding the ongoing impact of COVID-19.

On April 1, 2020, we announced our comprehensive action plan in response to the COVID-19 health crisis, which combined both health and safety as well as cost-saving initiatives. Measures taken included, among other things, the temporary closure of design centers and manufacturing facilities, the furlough of 70% of our global workforce, the decision by our CEO to temporarily forego his salary through June 30, 2020, a temporary reduction in salaries of up to 40% for all senior management and up to 20% for other salaried employees through June 30, 2020, a temporary reduction of 50% in the cash compensation of the Company’s directors through June 30, 2020, the elimination of all non-essential operating expenses, a delay of capital expenditures, the temporary suspension of the regular quarterly dividend and temporarily halted the share repurchase program.

On April 22, 2020, we issued a press release providing business updates, including an update to our COVID-19 action plan which emphasized our continued focus on the health, safety and well-being of our associates, our customers, and the communities in which we operate. Our update emphasized the continued evaluation of plans and timing as it related to the planned reopening of our design centers and to restarting production in our North American manufacturing plants.

On May 11, 2020, we reported our fiscal 2020 third quarter results and provided an update on our COVID-19 action plan. In addition to the financial results disclosed in our press release, we also announced that we began reopening design centers in a number of U.S. states since May 1, 2020 and began resuming production in some of its North American manufacturing plants in a limited capacity to work through existing backlog and to be in a position to service expected demand as the economy begins to reopen for business. We further announced that our distribution and home delivery centers were open and making home deliveries.

On August 4, 2020, we announced that all of our Company-operated retail design centers reopened, including 14% open by appointment only. We also resumed production in our North American manufacturing plants during the second half of our fiscal 2020 fourth quarter, some in a limited capacity, and expect to work through existing order backlog and ramp up to full production by the end of August 2020. The temporary salary reductions were lifted, effective June 30, 2020, as planned. The Board of Directors also reinstated the regular quarterly dividend. Lastly, we have brought back approximately 56% of our associates previously furloughed in April 2020.

ETHAN ALLEN INTERIORS INC. AND SUBSIDIARIES

The COVID-19 crisis challenged our operations during fiscal 2020, but our associates did well in persevering through these challenges. Our primary focus was operating in a safe manner, for our associates and clients. As our design centers began to reopen, we implemented various mitigating and safety protocols recommended by the CDC guidelines for operating businesses safely. We established logistics for the supply of hand sanitizer and related dispensers, disinfectant cleaning supplies, masks and nitrile gloves, and we increased the cleaning frequency of our design centers and other facilities. As a result of these additional supplies and cleaning regimes based on the CDC’s safe business protocols, we incurred incremental costs during fiscal 2020. These costs, which were less than $1.0 million, are reflected within our selling, general and administrative expenses. We expect to incur a similar level of expenses associated with safety and additional hygiene measures on an ongoing basis for the foreseeable future. For the safety of our associates in our design centers we require all associates and clients to wear masks. So far, we have been fortunate with very few cases of COVID-19 throughout our enterprise, which resulted in no disruptions to our operations.

We continue to manage the impact of the COVID-19 crisis on a daily basis. As of the date of this filing, we are unable to predict the ultimate impact COVID-19 will have on our financial operations in the near and long term remains unknown. The timing of any future actions in response to COVID-19 is largely dependent on the mitigation of the spread of the virus, status of government orders, directives and guidelines, recovery of the business environment, economic conditions, and consumer demand for our products.

Product

The majority of the products we sell are built by artisans in our North American plants. Most upholstery frames are hand-assembled and stitching is guided by hand. We select international partners who are as committed to quality and social responsibility as we are. All case goods frames are made with premium lumber and veneers. We use best-in-class construction techniques, including mortise and tenon joinery and four-corner glued dovetail joinery on drawers. We combine technology with personal service and maintain an up-to-date broad range of styles and custom options in keeping with today’s home decorating trends. These factors continue to define Ethan Allen, positioning us as a fashion leader in the home furnishing industry.

The interior of our design centers are organized to facilitate display of our product offerings, both in room settings that project the category lifestyle and by product grouping to facilitate comparisons of the styles and tastes of our customers. To further enhance the experience, technology is used to expand the range of products viewed by including content from our website and 3D digital images in applications used on large touch-screen flat panel displays.

Product Development

Using a combination of employees and designers, we design and build the majority of the products we sell. All of our products are Ethan Allen branded. This important facet of our vertically integrated business enables us to control the design specifications and establish consistent levels of quality across all our product programs. In addition to our six United States manufacturing facilities, we have two upholstery manufacturing plants in Mexico and a case goods manufacturing facility in Honduras. We selectively outsource the remaining 25% of our products, primarily from Asia. We carefully select our sourcing partners and require strict compliance with our specifications, quality and social responsibility standards. We believe that our strategic investments in our manufacturing facilities balanced with outsourcing from foreign and domestic suppliers will enable us to accommodate any significant future sales growth and allow us to maintain an appropriate degree of control over cost, quality and service to our customers.

Raw Materials and Other Suppliers

The most important raw materials we use in furniture manufacturing are lumber, veneers, plywood, hardware, glue, finishing materials, glass, laminates, steel, fabrics, foam, and filling material. The various types of wood used in our products include cherry, ash, oak, maple, prima vera, African mahogany, birch, rubber wood and poplar.

Fabrics and other raw materials are purchased both domestically and outside the United States . We have no significant long-term supply contracts and have sufficient alternate sources of supply to prevent disruption in supplying our operations. We maintain a number of sources for our raw materials, which we believe contribute to our ability to obtain competitive pricing. Lumber prices and availability fluctuate over time based on factors such as weather and demand. The cost of some of our raw materials such as foam and shipping costs are dependent on petroleum cost. Higher material prices, cost of petroleum, and costs of sourced products could have an adverse effect on margins.

Appropriate amounts of lumber and fabric inventory are typically stocked to maintain adequate production levels. We believe that our sources of supply for these materials are sufficient and that we are not dependent on any one supplier. We enter into standard purchase agreements with foreign and domestic suppliers to source selected products. The terms of these arrangements are customary for the industry and do not contain any long-term contractual obligations on our behalf. We believe we maintain good relationships with our suppliers.

ETHAN ALLEN INTERIORS INC. AND SUBSIDIARIES

Segments

We have strategically aligned our business into two reportable segments: Wholesale and Retail. Our operating segments are aligned with how the Company, including our chief operating decision maker, manages the business. These two segments represent strategic business areas of our vertically integrated enterprise that operate separately and provide their own distinctive services. This vertical structure enables us to offer our complete line of home furnishings and accents while controlling quality and cost. We evaluate performance of the respective segments based upon net sales and operating income. Inter-segment transactions result, primarily, from the sale of wholesale inventory to the retail segment, including the related profit margin. Financial information, including sales, operating income and long-lived assets related to our segments are disclosed in Note 19, Segment Information, of the notes to our consolidated financial statements included under Item 8 of this Annual Report on Form 10-K.

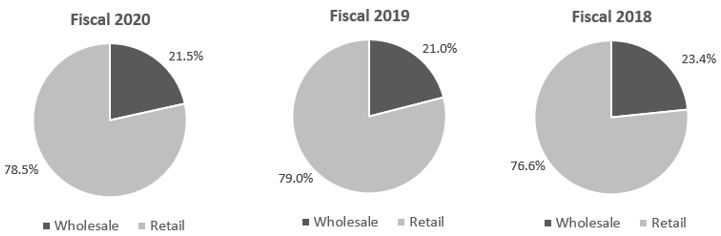

As of June 30, 2020, the Company operated 144 design centers (our retail segment) and our independent retailers operated 160 design centers. Our wholesale segment’s net sales include sales to our retail segment, which are eliminated in consolidation, and sales to our independent retailers and other unaffiliated third parties. Our retail segment net sales accounted for 78.5% of our consolidated net sales in fiscal 2020. Our wholesale segment net sales accounted for the remaining 21.5%.

The following charts depict net sales related to our reportable segments.

We believe that the demand for furniture generally reflects sensitivity to overall economic conditions, including consumer confidence, discretionary spending, housing starts, sales of new and existing homes, housing values, the level of mortgage refinancing, debt levels, retail trends and unemployment rates. For both our segments, the second and fourth quarters are historically the seasonally highest-volume sales quarters. However, during fiscal 2020, we experienced our largest sales volume quarter for our wholesale business during the first quarter while our retail segment had its highest sales volume during the second quarter. We believe this fiscal 2020 experience was not an indicator that our seasonal trends are changing and was primarily due to disruptions in the market caused by the COVID-19 pandemic in the second half of fiscal 2020.

Retail Segment

The retail segment, which accounted for 78.5% of net sales during fiscal 2020, sells home furnishings and accents to clients through a network of Company-operated design centers. Retail revenue is generated upon the retail sale and delivery of our products to our retail customers through our network of retail home delivery centers. Retail profitability reflects (i) the retail gross margin, which represents the difference between the retail net sales price and the cost of goods, purchased from the wholesale segment, and (ii) other operating costs associated with retail segment activities.

We measure the performance of our design centers primarily based on net sales and profitability on a comparable period basis. The frequency of our promotional events as well as the timing of the end of those events can affect the comparability of net sales during a given period. Due to the nature of the business in which the retail segment operates, there are no customer concentration risks.

The retail segment’s product line revenue, expressed as a percentage of net sales, is comprised of approximately 48% in upholstered products, 29% case goods and the remaining 23% in home accents and other.

During fiscal 2020, we acquired one new design center in the United States from an independent retailer, opened two and closed three locations, which is net of seven relocations. The geographic distribution of retail design center locations is disclosed under Item 2, Properties, contained in Part I of this Annual Report on Form 10-K.

ETHAN ALLEN INTERIORS INC. AND SUBSIDIARIES

Wholesale Segment

The wholesale segment, which accounted for 21.5% of net sales during fiscal 2020, is principally involved in the development of the Ethan Allen brand and encompasses all aspects of design, manufacturing, sourcing, marketing, sale and distribution of our broad range of home furnishings and accents. Wholesale revenue is generated upon the sale and shipment of our products to our retail network of independently operated design centers, Company-operated design centers and other contract customers. Sales to ten of our largest customers accounted for 27% of revenues within our wholesale segment during fiscal 2020.

Within the wholesale segment, we maintain revenue information according to each respective product line (i.e. case goods, upholstery and home accents). Case goods include items such as beds, dressers, armoires, tables, chairs, buffets, entertainment units, home office furniture and wooden accents. Upholstery items include sleepers, recliners and other motion furniture, chairs, ottomans, custom pillows, sofas, loveseats, cut fabrics and leather. Skilled artisans cut, sew and upholster custom-designed upholstery items which are available in a variety of frame, fabric and trim options. Home accent items include window treatments and drapery hardware, wall décor, florals, lighting, clocks, mattresses, bedspreads, throws, pillows, decorative accents, area rugs, wall coverings and home and garden furnishings.

Wholesale profitability includes (i) the wholesale gross margin, which represents the difference between the wholesale net sales price and the cost associated with manufacturing and/or sourcing the related product, and (ii) other operating costs associated with wholesale segment activities.

The wholesale segment’s product line revenue, expressed as a percentage of net sales, is comprised of approximately 48% in upholstered products, 34% case goods and the remaining 18% in home accents and other.

As of June 30, 2020, our wholesale backlog was $63.8 million, up 37.6% compared with $46.4 million a year ago. Our backlog increased due to a 17.5% increase in wholesale orders booked in June 2020 combined with our inability to quickly return our manufacturing plants to desired staffing levels due to COVID-19 related restrictions, including safe workplace environment requirements and social distancing. These restrictions have kept production and net shipments below the prior year rate. The strong product demand, coupled with ramping up manufacturing, has also resulted in extended lead times between order and delivery and slower-than-normal delivered sales. We resumed production in our North American manufacturing plants during the second half of the fourth quarter of fiscal 2020, some in a limited capacity, and expect to work through this existing order backlog during the first half of fiscal 2021. Our wholesale backlog fluctuates based on the timing of net orders booked, manufacturing schedules and efficiency, the timing of sourced product receipts, the timing and volume of wholesale shipments, and the timing of various promotional events.

Our independent retailers are required to enter into license agreements with us, which (i) authorize the use of certain Ethan Allen trademarks and (ii) require adherence to certain standards of operation, including a requirement to fulfill related warranty service agreements. We are not subject to any territorial or exclusive retailer agreements in North America.

The geographic distribution of manufacturing and distribution locations is disclosed under Item 2, Properties, contained in Part I of this Annual Report on Form 10-K.

Talent

Since our founding, we have built a collaborative culture that recognizes and rewards innovation and offers employees a variety of opportunities and experiences. After almost nine decades in business, the name Ethan Allen is well known and highly regarded in the home furnishings marketplace. Our employees are vital to our success and are one of the main reasons we continue to execute at a high level. We believe our employees have an entrepreneurial spirit, a passion for style, a drive for excellence, outstanding communication skills and create a culture that embraces creativity, integrity, diversity, innovation and inclusion of people from all backgrounds. Our continued focus on making employee engagement a top priority will help us provide high quality products and services to our customers.

At June 30, 2020 our employee count totaled 3,369, a decrease from 4,736 a year ago. We are gratified with the work and focus of our teams during the unprecedented crisis caused by the ongoing COVID-19 pandemic. We have had to make many hard decisions including the furlough of approximately 70% of our global workforce in April 2020. Fortunately, we have been able to bring many associates back with 56% of them having returned to work by June 30, 2020. The majority of our employees are employed on a full-time basis and we believe we maintain good relationships with our employees. None of our employees are represented by unions or collective bargaining agreements.

ETHAN ALLEN INTERIORS INC. AND SUBSIDIARIES

Customer Service Offerings

We offer numerous customer service programs, each of which has been developed and introduced to customers in an effort to make their shopping experience easier and more enjoyable.

Gift Card. This program allows customers to purchase and redeem gift cards through our website or at any participating retail design center, which can be used for any of our products or services.

Ethan Allen Consumer Credit. The Ethan Allen Platinum Card consumer credit program offers customers a menu of custom financing options. Financing offered through this program is administered by a third-party financial institution and is granted to our customers on a non-recourse basis to the Company. Customers may apply for an Ethan Allen Platinum card at any participating design center or online at ethanallen.com.

Marketing

“We Make the American HomeTM,” Ethan Allen’s marketing mission statement, drives home our core brand values: Quality and Craftsmanship, Complimentary Design Service and Premier In-Home Delivery. We amplify those values through a dynamic brand story told across three predominant lifestyles—Classic, Country/Coastal and Modern—thus promoting a broad, yet curated range of products, resulting in a superlative combination of product value and personal service.

By adopting a fresh, ever-evolving creative approach, we have reinvigorated our brand, enhancing its desirability and visibility while driving both new and repeat client traffic to our approximately 300 design centers network-wide and to our primary website, ethanallen.com. We consider the breadth and depth of our product offerings, enhanced by the countless custom options we offer, to be a key competitive advantage.

Using our fully integrated customer relationship management system, we create personalized customer journeys, targeted communications, and retargeting campaigns. We develop persuasive, aspirational, and relevant messaging, and we convey it through a variety of media including direct mail, national and local TV and radio, digital and social channels and email marketing, which has positively impacted both traffic and conversion nationwide.

As our e-commerce sales continue increasing at double-digit rates, we have implemented conversion rate optimization updates on both ethanallen.com and ethanallen.ca. We also invest in targeted search engine optimization and paid search marketing, for both national and local markets, driving both referral traffic to our website and physical traffic to our design centers. In addition, improved on-site search capabilities, expanded Live Chat services, online appointment booking capability, and product listing and display page enhancements have elevated the user experience.

We have increased brand visibility on Facebook, Instagram, and Pinterest, with a greater emphasis on visual and video-driven content. Both paid social media campaigns and organic social media presence have helped us grow our social following by 20%, drive revenue, and take a more prominent place in the cultural conversation.

By investing in digital design technologies, we have expanded our virtual design appointment capabilities. EA inHome®, an augmented reality mobile app, empowers clients to preview Ethan Allen products in their homes, at scale, in a variety of fabrics and finishes. With the 3D Room Planner, our designers generate both 2D floor plans and immersive, incredibly realistic 3D walk-throughs of the designs they create. These technologies have been pivotal to our ability to serve clients remotely during the ongoing COVID-19 pandemic. Clients can shop with confidence, knowing that they’re investing in beautiful, cohesive room designs and pieces that suit their space.

Once clients reach the point of purchase, we offer enticing financing options through the Ethan Allen Platinum Card, a third party-administered consumer credit program. Designed to make Ethan Allen accessible to everyone, the card launched successfully nationwide and continues to attract both new and recurring clients, driven by a recent offer of 0% APR for 48-months, which aided conversion and order size.

Competition

We believe the home furnishings industry competes primarily on the basis of product styling and quality, personal service, prompt delivery, product availability and price. We further believe that we effectively compete on the basis of each of these factors and that, more specifically under our vertical structure, our complimentary interior design service, direct manufacturing, white glove delivery service, product presentations, and website create a competitive advantage, further supporting our mission of providing customers with a complete home decorating and design solution. We also believe that we differentiate ourselves further with the quality of our interior design service through our intensive training and the caliber of our design consultants. Our objective is to continue to develop and strengthen our retail network by (i) expanding the Company-operated retail business through the repositioning and opening of new design centers, (ii) obtaining and retaining independent retailers, encouraging such retailers to expand their business through the opening or relocation of new design centers with the objective of increasing the volume of their sales, (iii) further expanding our sales network through our independent design associates and realtor referral programs, and (iv) further expanding our ecommerce.

ETHAN ALLEN INTERIORS INC. AND SUBSIDIARIES

Retail Design Centers

We continue to strengthen the Ethen Allen brand with many initiatives, including the opening of new design centers and relocating or consolidating certain existing design and home delivery centers, regularly updating presentations and floor plans, and strengthening of the qualifications of our designers through training and certification. Combining technology with personal service in our design centers has allowed us to reduce the size of our design centers. In the past five years, we have either opened or relocated a total of 29 new design centers that have an average size of approximately 9,300 square feet. These smaller footprint design centers reflect our direction as we move forward in repositioning our retail design centers. These new and relocated design centers also reflect our shift from destination and shopping mall locations to lifestyle centers that better project our brand and offer increased traffic opportunities.

Ethan Allen design centers are typically located in busy retail settings as freestanding destinations or as part of town centers, lifestyle centers, suburban strip malls or shopping malls, depending upon the real estate opportunities in a particular market. Our 144 Company-operated retail design centers average approximately 15,000 square feet in size with 59% of them ranging between 10,000 and 20,000 square feet, while 25% being less than 10,000 square feet and the remaining 16% being greater than 20,000 square feet. During the past 10 years, 52% of our design centers are new or have been relocated.

We strive to maintain consistency of presentation throughout our retail design centers through a comprehensive set of standards and display planning assistance. These interior display design standards enable each design center to present a high-quality image by using focused lifestyle settings and select product category groupings to display our products and information to facilitate design solutions and to educate consumers. We also create a consistent brand projection through our exterior facades and signage.

Distribution and Logistics

We distribute our products through four distribution centers, owned by the Company, strategically located in North Carolina, Oklahoma, and Virginia. These distribution centers provide efficient cross-dock operations to receive and ship product from our manufacturing facilities and third-party suppliers to our retail network of Company and independently operated retail home delivery centers. Retail home delivery centers prepare products for delivery into customers’ homes. At June 30, 2020, our Company-operated retail design centers were supported by 16 Company-operated retail home delivery centers and 10 home delivery centers operated by third parties.

While we manufacture to custom order the majority of our products, we also stock certain case goods, upholstery and home accents to provide for quick delivery of in-stock items and to allow for more efficient production runs. We utilize independent carriers to ship our products.

Our practice has been to sell our products at the same delivered cost to all Company and independently operated design centers throughout the United States, regardless of their shipping point. This policy creates pricing credibility with our wholesale customers while providing our retail segment the opportunity to achieve more consistent margins by removing fluctuations attributable to the cost of shipping. Further, this policy eliminates the need for our independent retailers to carry significant amounts of inventory in their own warehouses. As a result, we obtain more accurate consumer product demand information.

Environmental Sustainability and Social Responsibility

We continue to be focused on environmental and social responsibility while incorporating uniform social, environmental, health and safety programs into our global manufacturing standards.

Our environmental (green) initiatives include but are not limited to the use of responsibly harvested Appalachian woods, and water-based finishes and measuring our carbon footprint, greenhouse gases and recycled materials from our operations. We have eliminated the use of heavy metals and hydrochlorofluorocarbons in all packaging. Our mattresses and custom upholstery use foam made without harmful chemicals and substances. We have implemented the Enhancing Furniture’s Environmental Culture (“EFEC”) environmental management system sponsored by the American Home Furnishing Alliance (“AHFA”) at all our domestic manufacturing, distribution and home delivery center facilities, and have expanded these efforts to our retail design centers, which have now been registered in EFEC. Our Mexico and Honduras facilities are also registered under the AHFA's EFEC program. Our United States manufacturing, distribution and home delivery centers have also achieved Sustainable by Design (“SBD”) registration status under the EFEC program. SBD provides a framework for home furnishings companies to create and maintain a corporate culture of conservation and environmental stewardship by integrating socio-economic policies and sustainable business practices into their manufacturing operations and sourcing strategies.

ETHAN ALLEN INTERIORS INC. AND SUBSIDIARIES

The Company requires its sourcing facilities that manufacture Ethan Allen branded products to implement a labor compliance program and meet or exceed the standards established for preventing child labor, involuntary labor, coercion and harassment, discrimination, and restrictions to freedom of association. These facilities are also required to provide a safe and healthy environment in all workspaces, compliance with all local wage and hour laws and regulations, compliance with all applicable environmental laws and regulations, and are required to authorize Ethan Allen or its designated agents (including third-party auditing companies) to engage in monitoring activities to confirm compliance.

We work to ensure our products are safe in our customers’ homes through responsible use of chemicals and manufacturing substances.

Intellectual Property

We currently hold, or have registration applications pending for, numerous trademarks, service marks and copyrights for the Ethan Allen name, logos and designs in a broad range of classes for both products and services in the United States and in many foreign countries. In addition, we have registered, or have applications pending for certain of our slogans utilized in connection with promoting brand awareness, retail sales and other services and certain collection names. In addition, we have registered and maintain the internet domain name of ethanallen.com. We view such trademarks, logos, service marks and domain names as valuable assets and have an ongoing program to diligently monitor and defend, through appropriate action, against their unauthorized use.

Government Regulation

The Company is subject to reporting requirements, disclosure obligations and other recordkeeping requirements of the Securities and Exchange Commission (“SEC”) and the various local authorities that regulate each location in which we operate.

Corporate Contact Information

Ethan Allen’s principal executive office is in Danbury, Connecticut.

| |

●

|

Mailing address of the Company’s headquarters: 25 Lake Avenue Ext., Danbury, Connecticut 06811-5286

|

| |

●

|

Telephone number: +1 (203) 743-8000

|

| |

●

|

Website address: ethanallen.com

|

Available Information

Information contained in our Investor Relations section of our website at https://ir.ethanallen.com is not part of this Annual Report on Form 10-K. Information that we furnish or file with the SEC, including our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K or exhibits included in these reports are available for download, free of charge, on our Investor Relations website soon after such reports are filed with or furnished to the SEC. Our SEC filings, including exhibits filed therewith, are also available on the SEC’s website at sec.gov.

Information about our Executive Officers

Listed below are the name, age, and current position for each of our executive officers as of the date of this Annual Report on Form 10-K.

M. Farooq Kathwari*, age 75

| |

●

|

Chairman of the Board, President and Chief Executive Officer since 1988

|

Daniel M. Grow, age 74

| |

●

|

Senior Vice President, Business Development since February 2015

|

| |

●

|

Vice President, Business Development from 2009 to 2015

|

Rodney A. Hutton, age 52

| |

●

|

Chief Marketing Officer since joining the Company on a full-time basis in January 2020

|

| |

●

|

Consultant to Ethan Allen from September 2019 to January 2020

|

| |

●

|

Previously held senior marketing, brand management and merchandising roles in a number of leading enterprises including Ralph Lauren, Giorgio Armani, Karl Lagerfeld, Ann Klein and Iconix Brand Group

|

ETHAN ALLEN INTERIORS INC. AND SUBSIDIARIES

Eric D. Koster, age 73

| |

●

|

Vice President, General Counsel and Secretary since April 2013

|

| |

●

|

Private practice prior to joining the Company in April 2013

|

Christopher Robertson, age 51

| |

●

|

Vice President, Logistics and Service since January 2016

|

| |

●

|

Director, Operations Support since May 2011

|

Clifford Thorn, age 68

| |

●

|

Vice President, Upholstery Manufacturing since May 2001

|

Corey Whitely, age 60

| |

●

|

Executive Vice President, Administration, Chief Financial Officer and Treasurer since July 2014

|

| |

●

|

Executive Vice President, Operations from October 2007 through July 2014

|

Michael Worth, age 53

| |

●

|

Vice President, Case Goods Manufacturing since December 2016

|

| |

●

|

Regional Operations Manager, Case Goods since February 2004

|

* Mr. Kathwari is the only one of our executive officers who operates under a written employment agreement.

Additional Information

Additional information with respect to the Company’s business is included in the following pages and is incorporated herein by reference:

| |

Page

|

|

Five-Year Summary of Selected Financial Data

|

26

|

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

27

|

|

Quantitative and Qualitative Disclosures about Market Risk

|

43

|

|

Note 1 to Consolidated Financial Statements entitled Organization and Nature of Business

|

52

|

|

Note 19 to Consolidated Financial Statements entitled Segment Information

|

76

|

ETHAN ALLEN INTERIORS INC. AND SUBSIDIARIES

ITEM 1A. RISK FACTORS

The following risks could materially and adversely affect our business, financial condition, cash flows, results of operations and the trading price of our common stock could decline. These risk factors do not identify all risks that we face; our operations could also be affected by factors that are not presently known to us or that we currently consider to be immaterial to our operations. Investors should also refer to the other information set forth in this Annual Report on Form 10-K, including Management’s Discussion and Analysis of Financial Condition and Results of Operations and our financial statements including the related notes. Investors should carefully consider all risks, including those disclosed, before making an investment decision.

The ongoing global COVID-19 pandemic has and may continue to materially adversely affect our business, our results of operations and our overall financial performance.

The ongoing global COVID-19 pandemic has negatively impacted the world economy, disrupted financial markets and international trade, resulted in increased unemployment levels and significantly impacted global supply chains, all of which have negatively affected and continue to materially negatively affect the retail industry and the Company’s business. COVID-19 continues to spread both in the U.S. and globally, and related government and private sector mitigation efforts, including travel restrictions, border closings, restrictions on public gatherings, especially when congregating in heavily populated areas, such as malls and shopping centers, shelter-in-place restrictions and limitations on business, including requiring reduction of operating hours and forced temporary closures of non-essential retailers and other businesses, have adversely affected and are expected to continue to adversely affect our business operations, financial condition and liquidity. In particular, the continued spread of COVID-19 and efforts to contain the virus:

| |

●

|

resulted in significant declines in net sales across our segments and could continue to impact customer demand for our products and services and customer spending levels, including a sustained long-term adverse impact on future foot traffic to our retail locations as a result of any changes to customer shopping patterns and behaviors, such as consumer willingness to visit physical retail locations, including our design centers;

|

| |

●

|

continue to reduce the availability and productivity and impact the health and well-being of our employees, customers and business partners;

|

| |

●

|

continue to cause us to experience a material increase in costs as a result of sustained mitigation measures, delayed payments from our customers and uncollectable accounts;

|

| |

●

|

continue to cause disruptions in the availability of and timely delivery of materials used in our operations;

|

| |

●

|

may materially and adversely impact our liquidity position and cost of, and ability to access, funds from financial institutions and capital markets; and

|

| |

●

|

cause other unpredictable events that we currently cannot anticipate.

|

We have instituted measures to ensure our supply chain remains open to us; however, there has been some recent raw material supply chain challenges related to suppliers negatively impacted by COVID-19 shutdowns and shipping delays. These global supply chain challenges could continue and in turn materially adversely impact our manufacturing production and fulfillment of backlog. Furthermore, any significant reduction in consumer willingness to visit our design centers, levels of consumer spending, employee willingness to work in our design centers, or additional closures of our design centers or distribution centers, relating to COVID-19 or its impact on the economy, consumer sentiment or health concerns, already resulted and could result in a further loss of revenues, profits, cash flows, and other materially impactful effects on our business and operations. Our customers may have been, and may continue to be negatively affected by layoffs or work reductions as a result of the global economic downturn caused by COVID-19, which may have negatively impacted, and could continue to negatively impact demand for our products as customers delay or reduce discretionary purchases. Any significant reduction in customer traffic and spending at our design center, caused directly or indirectly by COVID-19, would continue to result in a loss of revenue and profits and could result in other material adverse effects.

In addition, we implemented work-from-home policies for certain employees. These working arrangements as well as other related restrictions including severe limitations on travel may have an impact on our operations and management effectiveness. Although we have technology and other resources to support these new work requirements, there can be no assurance that we will not suffer material risks to our business, operations, productivity and results of operations as a result of these restrictions. If a significant percentage of our workforce is unable to work, including because of illness or travel or government restrictions in connection with COVID-19, our retail, distribution and manufacturing operations may be negatively impacted, potentially materially adversely affecting our business, liquidity, financial condition or results of operations.

ETHAN ALLEN INTERIORS INC. AND SUBSIDIARIES

Although our distribution centers were fully operational as of the date of filing of this Annual Report, governmental mandates or illness or absence of a substantial number of distribution center employees could require that we temporarily close one or more of our distribution centers, or may prohibit or significantly limit us, or our third party logistics providers, from delivering to our customers and our design centers, which would complicate or prevent our fulfilling orders and, once our design centers reopen, would complicate or prevent our ability to supply merchandise to these design centers. Further, although we continue to implement strong physical and cyber-security measures to ensure that our business operations remain functional and to ensure uninterrupted service to our customers, our systems and our operations remain vulnerable to cyber-attacks and other disruptions due to the fact that a significant portion of our employees work remotely as a result of the ongoing COVID-19 crisis, and we cannot be certain that our mitigation efforts will be effective.

The extent of the impact of COVID-19 on our operational and financial performance will depend on future developments, including the duration and spread of the virus and related restrictions. At this time, given the uncertainty of the lasting effect of COVID-19, the financial impact on the world economy, and in particular, our business, cannot be determined. Further, despite our efforts to manage various impacts, the situation surrounding COVID-19 remains fluid and the potential for a material impact on our results of operations, financial condition and liquidity increases the longer the virus impacts activity levels in the U.S. and globally. The ultimate impact of the COVID-19 pandemic depends on factors beyond our knowledge or control, including the duration and severity of the COVID-19 outbreak as well as third-party actions taken to contain its spread and mitigate its public health effects. Therefore, we currently cannot estimate with any degree of certainty the potential impact to our financial position, results of operations and cash flows.

We may require funding from external sources, which may not be available at the levels we require, or may cost more than we expect, and, as a consequence, our expenses and operating results could be negatively affected.

Our liquidity could be further negatively impacted if the COVID-19 pandemic continues to persist for a significant period of time and we may be required to pursue additional sources of financing to obtain working capital, maintain appropriate inventory levels and meet our financial obligations. Depending on the continued impact of the crisis, further actions may be required to improve our cash position and capital structure. Concerns over the economic impact of the COVID-19 pandemic have caused extreme volatility in financial and capital markets, which has adversely impacted our stock price and may materially adversely affect our ability to access capital markets.

We regularly review and evaluate our liquidity and capital needs. We believe that our available cash, cash equivalents and cash flow from operations will be sufficient to finance our operations and expected capital requirements for at least the next 12 months. However, we might experience periods during which we encounter additional cash needs, and we might need additional external funding to support our operations.

In the event we require additional liquidity from our lenders, such funds may not be available to us on acceptable terms, or at all. In addition, in the event we were to breach any of our financial covenants, our banks would not be required to provide us with additional funding, or they may require us to renegotiate our existing credit facility on less favorable terms. In addition, we may not be able to renew our letters of credit that we use to help pay our suppliers, on terms that are acceptable to us, or at all, as the availability of credit facilities may become limited. Further, the providers of such credit may reallocate the available credit to other borrowers. If we are unable to access additional credit at the levels we require, or the cost of credit is greater than expected, it could adversely affect our operating results.

Declines in certain economic conditions, which impact consumer confidence and consumer spending, could negatively impact our sales, results of operations and liquidity.

The furniture industry and our business is particularly sensitive to declines in general economic conditions and to uncertainty regarding future economic prospects, including the current and evolving negative economic impact of the COVID-19 pandemic. Our principal products are consumer goods that may be considered postponable purchases. Economic downturns and prolonged negative conditions in the economy could affect consumer spending habits by decreasing the overall demand for discretionary items, including home furnishings. Consumer purchases of discretionary items, including our products, generally decline during periods when disposable income is limited, unemployment rates increase or there is uncertainty about future economic prospects. In addition, changes in interest rates, consumer confidence, new housing starts, existing home sales, the availability of consumer credit and broader national or geopolitical factors also impact our business. We have seen negative effects on certain of these measures due to the COVID-19 pandemic. Consumer spending could remain depressed for an extended time and improvement in our sales could lag behind a general economic recovery as consumers may postpone the purchase of relatively higher-cost discretionary items.

ETHAN ALLEN INTERIORS INC. AND SUBSIDIARIES

An overall decline in the health of the economy and consumer spending may affect consumer purchases of discretionary items, which could reduce demand for our products and materially harm our sales, profitability and financial condition.

Our business depends on consumer demand for our products and, consequently, is sensitive to a number of factors that influence general consumer spending on discretionary items in particular. Factors influencing consumer spending include general economic conditions, consumer disposable income, fuel prices, recession and fears of recession, unemployment, war and fears of war, inclement weather, availability of consumer credit, consumer debt levels, conditions in the housing market, interest rates, sales tax rates and rate increases, inflation, civil disturbances and terrorist activities, foreign currency exchange rate fluctuations, consumer confidence in future economic and political conditions, natural disasters, and consumer perceptions of personal well-being and security, including health epidemics or pandemics, such as the COVID-19 pandemic. For example, demand for certain of our products decreased during the fourth quarter of fiscal 2020 as a result of the economic impact of the COVID-19 pandemic and weakened consumer confidence in the economy and financial markets. Prolonged or pervasive economic downturns could slow the pace of new design center openings or cause current design centers to temporarily or permanently close. Adverse changes in factors affecting discretionary consumer spending have reduced and may continue to further reduce consumer demand for our products, thus reducing our sales and harming our business and operating results.

Historically, the home furnishings industry has been subject to cyclical variations in the general economy and to uncertainty regarding future economic prospects. Should the current economic recovery falter or the current recovery in housing starts to stall, consumer confidence and demand for home furnishings could deteriorate, which could adversely affect our business through its impact on the performance of our Company-owned design centers, as well as on our independent licensees and the ability of a number of them to meet their obligations to us.

Our business and results of operations are affected by international, national and regional economic conditions. Regional economic conditions in the United States and in other regions of the world where we have a concentration of design centers such as Canada or China, may have a greater impact on the Company compared to economic conditions in other parts of the world where we have lesser concentration of design centers. An economic downturn of significance or extended duration could adversely affect consumer demand and discretionary spending habits and, as a result, our business performance, profitability, and cash flows.

Other financial or operational difficulties due to competition may result in a decrease in our sales, earnings, and liquidity.

The residential furniture industry is highly competitive and fragmented. We currently compete with many other manufacturers and retailers, including online retailers, some of which offer widely advertised products, and others, several of which are large retail furniture dealers offering their own store-branded products. Competition in the residential furniture industry is based on quality, style of products, perceived value, price, service to the customer, promotional activities, and advertising. The highly competitive nature of the industry means we are constantly subject to the risk of losing market share, which would likely decrease our future sales, earnings, and liquidity.

A significant shift in consumer preference toward purchasing products online could have a materially adverse impact on our sales and operating margin.

A majority of our business relies on physical design centers that merchandise and sell our products and a significant shift in consumer preference toward purchasing products online could have a materially adverse impact on our sales and operating margin. In the past year we have experienced lower traffic to our company-owned design centers, similar to other furniture retailers, as consumers have shifted to purchasing more furniture product online. The COVID-19 pandemic has accelerated the shift to online furniture purchases by changing customer shopping patterns and behaviors, including decreased consumer willingness to visit physical retail locations. We are attempting to meet consumers where they prefer to shop by expanding our online capabilities and improving the user experience at ethanallen.com to drive more traffic to both our online site and our physical design centers.

Rapidly evolving technologies are altering the manner in which the Company and its competitors communicate and transact with customers. Our strategy designed to adapt to these changes, in the context of competitors’ actions, customers adoption of new technology, and related changes in customer behavior, presents a specific risk in the event we are unable to successfully execute our plans or adjust them over time if needed. Further, unanticipated changes in pricing and other practices of competitors, including promotional activity, such as thresholds for free shipping and rapid price fluctuation enabled by technology, may adversely affect our performance.

ETHAN ALLEN INTERIORS INC. AND SUBSIDIARIES

Inability to maintain and enhance our brand may materially adversely impact our business.

Maintaining and enhancing our brand is critical to our ability to expand our base of customers and may require us to make substantial investments. Our advertising campaign utilizes television, direct mail, digital, newspapers, magazines and radio to maintain and enhance our existing brand equity. We cannot provide assurance that our marketing, advertising and other efforts to promote and maintain awareness of our brand will not require us to incur substantial costs. If these efforts are unsuccessful or we incur substantial costs in connection with these efforts, our business, operating results and financial condition could be materially adversely affected.

Failure to successfully anticipate or respond to changes in consumer tastes and trends in a timely manner could materially adversely impact our business, operating results and financial condition.

Sales of our products are dependent upon consumer acceptance of our product designs, styles, quality and price. We continuously monitor changes in home design trends through attendance at international industry events and fashion shows, internal marketing research, and regular communication with our retailers and design consultants who provide valuable input on consumer tendencies. However, as with all retailers, our business is susceptible to changes in consumer tastes and trends. Such tastes and trends can change rapidly and any delay or failure to anticipate or respond to changing consumer tastes and trends in a timely manner could materially adversely impact our business, operating results and financial condition.

Global and local economic uncertainty may materially adversely affect our manufacturing operations or sources of merchandise and international operations.

The current economic challenges in China, including global economic ramifications of the softening of the Chinese economy and trade agreement negotiations, may continue to put pressure on global economic conditions. This economic uncertainty, as well as other variations in global economic conditions such as fuel costs, wage and benefit inflation, and currency fluctuations, may cause inconsistent and unpredictable consumer spending habits, while increasing our own input costs. These risks resulting from global and local economic uncertainty could also severely disrupt our manufacturing operations, which could have a material adverse effect on our financial performance. We import a portion of our merchandise from foreign countries and operate manufacturing plants in Mexico and Honduras and retail design centers in Canada. As a result, our ability to obtain adequate supplies or to control our costs may be adversely affected by events affecting international commerce and businesses located outside the United States, including natural disasters, public health crises such as the ongoing COVID-19 pandemic, changes in international trade including tariffs, central bank actions, changes in the relationship of the United States dollar versus other currencies, labor availability and cost, and other governmental policies of the United States and the countries from which we import our merchandise or in which we operate facilities.

The United States, Mexico and Canada recently entered into a signed trade agreement called The United States - Mexico - Canada Agreement (“USMCA”) that has been ratified by all three countries. The USMCA will govern trade in North America and replaces the North American Free Trade Agreement (“NAFTA”). Compared to the previous NAFTA trade agreement, USMCA will increase environmental and labor regulations and will create incentives for more U.S. production of cars and trucks and impose a quota for Canadian and Mexico automotive production. Although we have determined that there have been no immediate effects on our operations with respect to USMCA, we cannot predict future developments in the political climate involving the United States, Mexico and Canada and thus these may have an adverse and material impact on our operations and financial growth.

Competition from overseas manufacturers and domestic retailers may materially adversely affect our business, operating results or financial condition.

Our wholesale business segment is involved in the development of our brand, which encompasses the design, manufacture, sourcing, sales and distribution of our home furnishings products, and competes with other United States and foreign manufacturers. Our retail network sells home furnishings to consumers through a network of independently operated and Company-operated design centers, and competes against a diverse group of retailers ranging from specialty stores to traditional furniture and department stores, any of which may operate locally, regionally, nationally or globally, as well as over the internet. We also compete with these and other retailers for retail locations as well as for qualified design consultants and management personnel. Such competition could adversely affect our future financial performance.

Industry globalization has led to increased competitive pressures brought about by the increasing volume of imported finished goods and components, particularly for case good products, and the development of manufacturing capabilities in other countries, specifically within Asia. The increase in overseas production has created over‐capacity for many manufacturers, including us, which has led to industry‐wide plant consolidation. In addition, because many foreign manufacturers are able to maintain substantially lower production costs, including the cost of labor and overhead, imported product may be capable of being sold at a lower price to consumers, which, in turn, could lead to some measure of further industry‐wide price deflation.

ETHAN ALLEN INTERIORS INC. AND SUBSIDIARIES

We cannot provide assurance that we will be able to establish or maintain relationships with sufficient or appropriate manufacturers, whether foreign or domestic, to supply us with selected case goods, upholstery and home accent items to enable us to maintain our competitive advantage. In addition, the emergence of foreign manufacturers has served to broaden the competitive landscape. Some of these competitors produce furniture types not manufactured by us and may have greater financial resources available to them or lower costs of operating. This competition could materially adversely affect our future financial performance.

Disruptions of our supply chain could have a material adverse effect on our operating and financial results.

Disruption of the Company’s supply chain capabilities due to trade restrictions, political instability, severe weather, natural disasters, public health crises such as the ongoing COVID-19 pandemic, terrorism, product recalls, labor supply or stoppages, the financial and/or operational instability of key suppliers and carriers, or other reasons could impair the Company’s ability to distribute its products. To the extent we are unable to mitigate the likelihood or potential impact of such events, there could be a material adverse effect on our operating and financial results.

Our number of manufacturing and logistics sites may increase our exposure to business disruptions and could result in higher transportation costs.

We have a limited number of manufacturing sites in our case goods and upholstery operations and consolidated our distribution network into fewer centers for both wholesale and retail segments. Our upholstery operations consist of two upholstery plants at our North Carolina campus and two plants in Mexico. The Company operates two manufacturing plants (Vermont and Honduras) and one sawmill, one rough mill and one lumberyard in support of our case goods operations. As a result of the consolidation of our manufacturing operations into fewer facilities, if any of our manufacturing or logistics sites experience significant business interruption, our ability to manufacture or deliver our products in a timely manner would likely be impacted. While we have long‐standing relationships with multiple outside suppliers of our raw materials and commodities, there can be no assurance of their ability to fulfill our supply needs on a timely basis. The consolidation to fewer locations has resulted in longer distances for delivery and could result in higher costs to transport products if fuel costs increase significantly.

Fluctuations in the price, availability and quality of raw materials could result in increased costs or cause production delays which might result in a decline in sales, either of which could materially adversely impact our earnings.

We use various types of wood, foam, fibers, fabrics, leathers, and other raw materials in manufacturing our furniture. Certain of our raw materials, including fabrics, are purchased domestically as well as outside North America. Fluctuations in the price, availability and quality of raw materials could result in increased costs or a delay in manufacturing our products, which in turn could result in a delay in delivering products to our customers. For example, lumber prices fluctuate over time based on factors such as weather and demand, which, in turn, impact availability. Production delays or upward trends in raw material prices could result in lower sales or margins, thereby materially adversely impacting our earnings.