Exhibit 99.1

The information contained in this preliminary offering memorandum is not complete and may be changed. We may not sell these notes until the offering memorandum is delivered in final form. This preliminary offering memorandum is not an offer to sell these notes and is not soliciting an offer to buy these notes in any state where the offer or sale is not permitted.

Subject to completion (Dated September 21, 2005)

Preliminary offering memorandum Strictly confidential

![]()

Ethan Allen Global, Inc.

$200,000,000

% Senior Notes due 2015

Issue price:

Interest payable and

The notes will bear interest at a rate of % per year and will mature on September , 2015. We will pay interest on the notes on and of each year, beginning . We may redeem the notes at our option in whole or in part at any time at the redemption prices described herein.

The notes will be fully, unconditionally and irrevocably guaranteed on a senior unsecured basis by our public parent company, Ethan Allen Interiors Inc., and by certain of our subsidiaries, including Ethan Allen Retail, Inc., Ethan Allen Operations, Inc. and Ethan Allen Realty, LLC, which hold a substantial majority of our assets, and Lake Avenue Associates, Inc. and Manor House, Inc. The guarantees will rank equally in right of payment with each respective guarantor's other unsecured and unsubordinated indebtedness and guarantees.

We will agree to consummate an exchange offer of the notes pursuant to an effective registration statement or cause resales of the notes to be registered pursuant to a shelf registration statement under the Securities Act. Additional interest is payable on the notes during any period in which we are not in compliance with our obligations to exchange or register the notes.

See "Risk factors" beginning on page 9 for a discussion of certain risks you should consider in connection with an investment in the notes.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the notes or determined if this offering memorandum is truthful or complete. Any representation to the contrary is a criminal offense.

The notes have not been registered under the Securities Act of 1933 or the securities laws of any other jurisdiction. Unless they are registered, the notes may be offered only in transactions that are exempt from registration under the Securities Act and state securities laws. Accordingly, we are offering the notes only to qualified institutional buyers under Rule 144A and outside the United States in compliance with Regulation S. The notes will not be listed on any securities exchange.

Delivery of the notes in book-entry form is expected to be made on or about .

| JPMorgan |

, 2005

You should rely only on the information contained or incorporated by reference in this offering memorandum. We have not, and the initial purchaser has not, authorized anyone to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. We are not, and the initial purchaser is not, making an offer to sell the notes in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing or incorporated by reference in this offering memorandum is accurate only as of the date on the front cover of this offering memorandum or the date of the document incorporated in this offering memorandum, as applicable. Our business, financial condition, results of operations and prospects may have changed since that date.

Table of contents

| |

Page |

|

|---|---|---|

| Notice to investors | i | |

| Notice to New Hampshire residents | iii | |

| SEC review | iii | |

| Forward-looking statements | iv | |

| Preliminary note | iv | |

| Summary | 1 | |

| Risk factors | 9 | |

| Use of proceeds | 17 | |

| Capitalization | 18 | |

| Selected financial data | 19 | |

| Management's discussion and analysis of financial condition and results of operations | 21 | |

| Business | 36 | |

| Management | 45 | |

| Description of the notes | 48 | |

| Book-entry; Delivery and form | 58 | |

| Exchange offer; Registration rights | 64 | |

| Certain U.S. federal income tax considerations | 68 | |

| Transfer restrictions | 73 | |

| Plan of distribution | 77 | |

| Legal matters | 80 | |

| Independent auditors | 80 | |

| Where you can find more information | 80 | |

| Incorporation of certain documents by reference | 81 |

This offering memorandum is a confidential document that we are providing only to prospective purchasers of the notes. You should read this offering memorandum before making a decision to purchase any notes. We have prepared this offering memorandum and we are solely responsible for its contents. You are responsible for making your own examination of us and your own assessment of the merits and risks of investing in the notes. The initial purchaser makes no representation or warranty, express or implied, as to the accuracy or completeness of any of the information set forth in this offering memorandum. You may contact us if you need any additional information.

By receiving this offering memorandum, you will be deemed to have agreed not to:

i

If you do not purchase any notes or this offering is terminated for any reason, you must return this offering memorandum to: Ethan Allen Global, Inc., Ethan Allen Drive, Danbury, Connecticut 06811, Attention: Investor Relations.

By purchasing any notes, you will be deemed to have acknowledged that:

This offering memorandum contains summaries, which we believe to be accurate, of the terms we consider to be material of certain documents, but reference is made to the actual documents. All such summaries are qualified in their entirety by this reference. See "Where you can find more information."

The notes are subject to restrictions on resale and transfer as described under "Transfer restrictions." By purchasing any notes, you will be deemed to have represented and agreed to all the provisions contained in that section of this offering memorandum. You should be aware that you may be required to bear the financial risks of investing in the notes for an indefinite period of time.

We are not providing you with any investment, legal, business, tax or other advice in this offering memorandum. You should consult with your own advisors, accountants and counsel as needed to assist you in making your investment decision and to advise you whether you are legally permitted to purchase the notes.

We are offering the notes in reliance on exemptions from the registration requirements of the Securities Act. These exemptions apply to offers and sales of securities that do not involve a public offering. The notes have not been recommended or approved by any federal, state or foreign securities or regulatory authorities, and no such securities or regulatory authority has passed on the accuracy or completeness of this offering memorandum. Any representation to the contrary is a criminal offense.

You must comply with all laws and regulations that apply to you in any place in which you buy, offer or sell any notes or possess this offering memorandum. You must also obtain any consents or approvals that you need in order to purchase the notes. We and the initial purchaser are not responsible for your compliance with these legal requirements.

This offering memorandum does not constitute an offer to sell or a solicitation of an offer to buy notes to any person in any jurisdiction where it is unlawful to make such an offer to sell or solicitation.

ii

We reserve the right to withdraw the offering of the notes at any time and we and the initial purchaser reserve the right to reject any commitment to subscribe for the notes in whole or in part and to allot to you less than the full amount of the notes subscribed for by you.

The distribution of this offering memorandum and the offer and sale of the notes may be restricted by law in certain jurisdictions. Persons into whose possession this offering memorandum or any of the notes come must inform themselves about, and observe, any such restrictions. See "Plan of distribution."

The notes will be available initially only in book-entry form. We expect that the notes will be issued in the form of one or more global certificates, which will be deposited with, or on behalf of, The Depository Trust Company ("DTC") and registered in its name or in the name of its nominee. Beneficial interests in the global certificates will be shown on, and transfers of beneficial interests in the global certificates will be effected through, records maintained by DTC and its participants. After initial issuance of the global certificates, notes in certificated form will be issued in exchange for the global certificates only as set forth in the indenture.

Notice to New Hampshire residents

NEITHER THE FACT THAT A REGISTRATION STATEMENT OR AN APPLICATION FOR A LICENSE HAS BEEN FILED UNDER CHAPTER 421-B OF THE NEW HAMPSHIRE REVISED STATUTES WITH THE STATE OF NEW HAMPSHIRE NOR THE FACT THAT A SECURITY IS EFFECTIVELY REGISTERED OR A PERSON IS LICENSED IN THE STATE OF NEW HAMPSHIRE CONSTITUTES A FINDING BY THE SECRETARY OF STATE THAT ANY DOCUMENT FILED UNDER RSA 421-B IS TRUE, COMPLETE AND NOT MISLEADING. NEITHER ANY SUCH FACT NOR THE FACT THAT AN EXEMPTION OR EXCEPTION IS AVAILABLE FOR A SECURITY OR A TRANSACTION MEANS THAT THE SECRETARY OF STATE HAS PASSED IN ANY WAY UPON THE MERITS OR QUALIFICATIONS OF, OR RECOMMENDED OR GIVEN APPROVAL TO, ANY PERSON, SECURITY OR TRANSACTION. IT IS UNLAWFUL TO MAKE, OR CAUSE TO BE MADE, TO ANY PROSPECTIVE PURCHASER, CUSTOMER OR CLIENT ANY REPRESENTATION INCONSISTENT WITH THE PROVISIONS OF THIS PARAGRAPH.

After completion of this offering, we have agreed to file a registration statement with the SEC as described in this offering memorandum. The SEC may review the registration statement and have comments thereon. It is possible that changes will be made to the description of our business and financial and other information included or incorporated by reference into this offering memorandum in response to SEC comments as well as developments after the date hereof. While we believe that the information included or incorporated by reference into this offering memorandum has been prepared in a manner that materially complies with published SEC regulations and is consistent with current practice, we cannot assure you that we will not be required to modify or reformulate such information. Any such modification or reformulation may be significant.

iii

This offering memorandum includes or incorporates by reference various forward-looking statements. All such forward-looking statements are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. In addition, we or our representatives have made or may make forward-looking statements on telephone or conference calls, by webcast or emails, in person, in presentations or written materials, or otherwise, orally or in writing. Such forward-looking statements are sometimes identified by words such as "will," "may," "project," "should," "would," "could," "target," "goal," "anticipate," "plan," "believe," "estimate," "expect," or "intend" or words or phrases of similar import. These forward-looking statements reflect our current expectations concerning future results and events, and actual results and events may differ materially.

All forward-looking statements are subject to various risks and uncertainties, including but not limited to: the effects of terrorist attacks or conflicts or wars involving the United States or its allies or trading partners; the effects of labor strikes; weather conditions that may affect sales; volatility in fuel, utility, transportation and security costs; changes in global or regional political or economic conditions, including changes in governmental and central bank policies; changes in business conditions in the furniture industry, including changes in consumer spending patterns and demand for home furnishings; effects of our brand awareness and marketing programs, including changes in demand for our products and acceptance of our new products; our ability to locate new store sites or negotiate favorable lease terms for additional stores or for expansion of existing stores; competitive factors, including changes in the products or marketing efforts of others; pricing pressures; fluctuations in interest rates and the cost, availability and quality of raw materials; those matters discussed in our SEC filings; and future decisions by us.

Occurrence of any of the events or circumstances described above could have a material adverse effect on our business, financial condition, results of operations or cash flows. No assurance can be given that any future transaction about which forward-looking statements may be made will be completed or as to the timing or terms of any such transaction. All subsequent written and oral forward-looking statements by or attributable to us or persons acting on our behalf are expressly qualified in their entirety by these factors. Except as otherwise required to be disclosed in periodic reports required to be filed by public companies with the SEC pursuant to the SEC's rules, we have no duty to update these statements.

On February 7, 2005, the Office of the Chief Accountant of the SEC issued a letter to the AICPA expressing its views regarding certain operating lease accounting issues and their application under accounting principles generally accepted in the United States. Our management subsequently initiated a review of our lease-related accounting practices and determined that the manner in which we accounted for (i) the amortization of leasehold improvements, (ii) landlord/tenant incentives (specifically, construction allowances) and (iii) the recognition of rent expense or income when the lease term contains periods of free or reduced rents (such as "rent holidays" and rent escalation provisions) were not consistent with the views expressed by the SEC and that certain previously filed financial statements required restatement. We filed amendments to our annual report on Form 10-K for the fiscal year ended June 30, 2004 (including all periods presented therein) and our quarterly reports on Form 10-Q for the interim periods ended September 30, 2004 and December 31, 2004 (including all periods presented therein) reflecting such restatements. All financial statement information included in this offering memorandum reflects such restatements.

iv

This summary highlights information contained elsewhere in this offering memorandum. It does not contain all of the information that you should consider before making a decision to invest in our notes. You should read carefully the entire offering memorandum and the documents incorporated by reference in this offering memorandum, including the considerations described under "Risk factors."

Except as otherwise set forth under "Description of the notes," references to "Ethan Allen" or "we," "us" or "our" mean Ethan Allen Interiors Inc. and its subsidiaries collectively or, if the context so requires, Ethan Allen Interiors Inc., Ethan Allen Global, Inc., Ethan Allen Retail, Inc., Ethan Allen Operations, Inc., Ethan Allen Realty, LLC, Lake Avenue Associates, Inc. or Manor House, Inc. as subsidiary guarantors or may mean any such entity, individually. References to "Ethan Allen Global" refer to the issuer of the notes.

We are one of the largest manufacturers and retailers of quality home furnishings and accessories, offering a full complement of home decorating solutions through the country's largest single-sourced, vertically-integrated network of home furnishing retail stores. As a vertically-integrated company, we design, manufacture, source, distribute, market, and sell a full range of home furnishings to a network of independently-owned and Ethan Allen-owned stores as well as coordinate related marketing and brand awareness efforts. We manufacture or assemble approximately 65% to 70% of our products at 12 manufacturing facilities, which consist of 6 case good plants (2 of which include separate sawmill operations), 5 upholstery plants and 1 home accent plant, all located in the United States. As of June 30, 2005, our products were sold through an exclusive international network of 313 retail stores in which the brand and the stores shared the same name, including 126 stores that we owned and operated and 187 stores that were owned and operated by independent retailers.

Leadership, Strategies and Strengths

With our unique vertically-integrated structure, we have established ourselves as an industry leader in the development of:

A Preferred Brand. Our product strategy has been to position our brand as a preferred brand offering superior quality and value while, at the same time, providing consumers with a

1

convenient, full-service, one-stop shopping solution for their home furnishing needs. To carry out this strategy, we continue to expand our reach to a broader consumer base by offering a diverse selection of functional and stylish value-priced product lines, many of which have been designed to effectively complement one another, reflecting the recent trend toward more eclectic home decorating. Founded in 1932, we have sold our products under the Ethan Allen brand name since 1937. Today, we believe that over 90% of consumers are aware of the Ethan Allen brand and associate it with style, quality, value and service. Since 2002, over 70% of our current product line is new, with the balance refined and enhanced through product redesign, additions, deletions, or finish changes.

International Network of Stores. As of June 30, 2005, our products were sold through an exclusive network of 313 retail stores, including 126 stores that we owned and operated and 187 stores that were owned and operated by independent retailers under license agreements. Our stores are located primarily in the United States and Canada, with a small number of independently-owned stores located throughout Asia, Canada, the Middle East, Europe, the West Indies and Africa.

Our Design Consultants. We have a network of over 3,000 design consultants and project managers and logistics staff who we believe provide our customers with the best home decorating service at no additional charge. Our design consultants receive training with respect to the distinctive design and quality features inherent in each of our products, which we believe helps to increase their performance and reduce costly turnover. We believe that our training allows the design consultants to more effectively communicate the elements of style and value that we believe differentiates us from our competitors. As such, we believe that our design consultants, and the complementary service they provide, create a distinct advantage over other home furnishing retailers.

One-Stop Shopping. We offer our customers the convenience of one-stop shopping by creating a comprehensive home furnishings solution. For example, our product collections consist of case goods, such as beds, dressers, armoires, night tables, dining room chairs and tables, buffets, sideboards, coffee tables, entertainment units, bathroom vanities and home office furniture. Our upholstery home furnishing products include sleepers, recliners, chairs, sofas, loveseats, cut fabrics and leather. Our home accessory products include window treatments, wall décor, lighting, clocks, wood accents, bedspreads, decorative accessories, area rugs, bedding, and home and garden furnishings. By offering such a wide array of products, we believe that we provide the consumer the convenience of one-stop shopping for all of their home furnishing needs.

Great Value. Over the past year, we introduced an innovative everyday pricing program, eliminating periodic sales events in lieu of an everyday best price on all of our product offerings, which we believe provides our customers with a better value and a more simplified shopping experience. The process through which we evolved to everyday best pricing gave us the opportunity to critically examine all facets of our business, making substantive changes where necessary, in order to more effectively carry out our solutions-based approach to home decorating. This new pricing strategy has enabled us to focus on streamlining our operations, reducing our costs, and reducing lead times to better serve consumers. We believe that this innovation demonstrates our commitment to differentiating ourselves through strategies focused on customer credibility and excellence in service.

2

Growth

Our drivers for growth include:

Monitoring Consumer Tastes. We continuously monitor consumer demand through internal marketing research and communication with our retailers and store design consultants who provide valuable input on consumer trends. As a result of this monitoring, we believe that we are able to react quickly to changing consumer tastes. Since 2002, over 70% of our current product line is new. We have redefined ourselves by offering more stylish product with added details, providing a higher level of quality, while offering a better value as reflected in our everyday best pricing. We believe that our two most important lifestyle categories in home furnishings are the Classic and the Casual. Our product lines are designed to reflect unique elements applicable to each lifestyle. To accomplish this, our collections consist of case goods and coordinated upholstered products and home accessories, each styled with its own distinct design characteristics. We believe that home accessories play an important role in our marketing program as they enable us to offer the consumer the convenience of one-stop shopping by creating a comprehensive home furnishing solution.

Opening New Retail Stores. We believe that we are an industry leader in designing stores that reflect the quality and style of the product inside while displaying the product in Classic and Casual lifestyles that reflect the way people aspire live. Our stores are located in busy urban settings as freestanding destination stores or as part of suburban strip malls, depending upon the real estate opportunities in a particular market. In the past five years, we and our independent retailers have opened 78 new stores, approximately 40% of which were relocations. In our corporate-owned stores, as a result of our relocation initiatives, we have experienced an increase in store traffic of as much as 148%, with an average increase of 91% over the last five years, and, in corresponding store sales of as much as 118%, with an average increase of 64% over the last five years. Over the next several years, we intend to continue to open new retail stores, relocate certain existing stores to prime retail locations in major markets, and where appropriate, acquire stores from, or sell stores to, independent retailers. In fiscal 2006, we anticipate opening approximately 20 new or relocated Ethan Allen branded stores. We will continue to promote the growth and development of our independent retailers by encouraging the relocation and expansion of their stores. Independent retailers, pursuant to license agreements, are authorized to use certain Ethan Allen service marks or trademarks and are required to adhere to certain standards of operations. We believe that these initiatives will be important growth drivers for us.

Our Vertically-Integrated Structure. We believe that our vertical integration gives us a significant competitive advantage in this dynamic environment as it allows us to design, manufacture, source, distribute, market, and sell our products through over 300 retail stores, the industry's largest single-sourced, vertically-integrated retail store network. Our vertical integration allows us to control the process from design and product development, domestic

3

manufacturing, balanced with foreign and domestic outsourcing, cost efficient logistics systems, to a coordinated marketing program. We further believe that we differentiate ourselves from the competition by focusing on our strategy of providing solutions to our customers, which we have been developing for over a decade. Our solutions include stylish, functional products, conveniently located stores with inspirational displays, coordinated products for one-stop shopping convenience, complementary design service, and free home delivery. We believe that having seen our vertically-integrated model, several domestic manufacturers are attempting to implement single-brand retail stores. By leveraging our vertically-integrated operating structure and adhering to a solutions-based approach, we believe that we have an opportunity to further differentiate ourselves as a preferred brand and as the most comprehensive and effective provider of home decorating solutions for consumers.

Marketing and Advertising Efforts. We have developed a highly coordinated, national advertising campaign designed to:

We have developed and implemented what we believe is the most coordinated national advertising campaign in the home furnishings industry using television, direct mail, newspapers, magazines and radio to market our products and services. Our direct mail magazine, which features our home furnishings collections in lifestyle settings, is one of our most important marketing tools, and reaches over 50 million households annually. We also use our website to drive additional business into the retail network through lead generation and information sourcing. We believe that our ability to coordinate our advertising efforts for all of our stores provides a competitive advantage over other home furnishing manufacturers and retailers. With an exclusive network of more that 300 retail stores participating in a uniform marketing approach and "speaking with one voice," we believe that we are better positioned to fulfill our brand promise on a consistent basis.

Competition

Industry Competition. The home furnishings industry is very large, highly competitive and fragmented. Consumer confidence and discretionary spending, particularly for home furnishings, have recently been impacted by rising fuel costs, increasing interest rates and the ongoing war in Iraq. The home furnishings industry competes primarily on the basis of product styling and quality, personal service, prompt delivery, product availability and price. Globalization, which represents the most notable change within the industry landscape in recent years, has led to increased competitive pressures. These competitive pressures have been brought about by the increasing volume of imported finished goods and components, particularly for case goods products. The continued development of manufacturing capabilities in other countries, specifically within Asia, has significantly increased overseas production capacities and created over-capacity for many U.S. manufacturers, including us, leading to the consolidation of our least efficient plants. In response to this, we have, in recent years, implemented a blended strategy, establishing relationships with certain manufacturers, both abroad and domestically, to source selected case goods, upholstery, and home accessory items. We intend to continue to balance our domestic production with opportunities to source from foreign and domestic manufacturers, as appropriate, in order to maintain our competitive advantage.

4

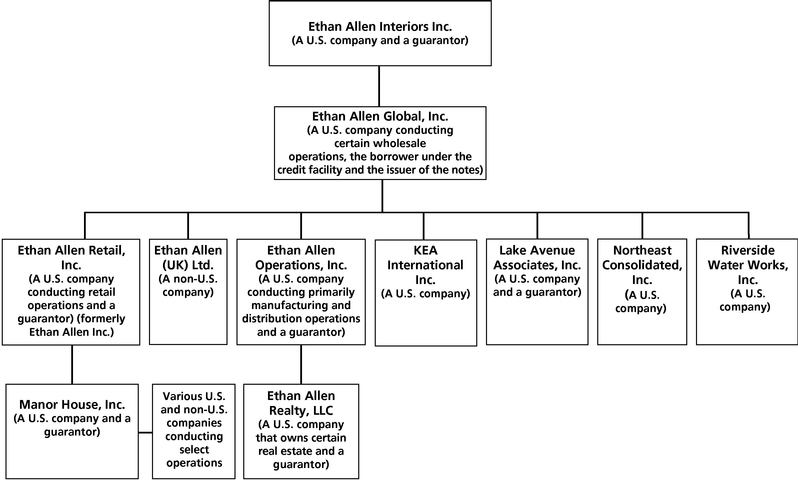

The following chart summarizes our current corporate organizational structure:

We hold, or have registration applications pending for, numerous trademarks, service marks and design patents for the Ethan Allen name, logos and designs in a broad range of classes for both products and services in the United States and in many foreign countries.

Ethan Allen Global, Inc. and Ethan Allen Interiors Inc., Ethan Allen Retail, Inc. and Ethan Allen Operations, Inc. and the other guarantors are Delaware corporations, except for Lake Avenue Associates, Inc., which is a Connecticut corporation and Ethan Allen Realty, LLC, which is a Delaware limited liability company. Our principal executive offices are located at Ethan Allen Drive, Danbury, Connecticut 06811, and our telephone number at that location is (203) 743-8000. We maintain a web site at http://www.ethanallen.com. The information contained on our web site is not part of this offering memorandum.

5

Issuer |

Ethan Allen Global, Inc. |

|||

Notes Offered |

$200,000,000 aggregate principal amount of % Senior Notes due 2015. |

|||

Maturity Date |

September , 2015. |

|||

Interest Payment Dates |

and of each year, beginning on , 2006. |

|||

Guarantees |

The notes will be guaranteed on a senior unsecured basis by Ethan Allen Interiors Inc., Ethan Allen Retail, Inc., Ethan Allen Operations, Inc., Lake Avenue Associates, Inc., Manor House, Inc. and Ethan Allen Realty, LLC. |

|||

Ranking |

The notes will rank senior to present and future subordinated debt and equally with present and future senior debt and obligations of Ethan Allen Global and each of the guarantors. |

|||

Optional Redemption |

We may redeem the notes in whole at any time or in part from time to time at the redemption prices described in this offering memorandum, plus accrued and unpaid interest to the date of redemption. |

|||

Certain Covenants |

The indenture will contain covenants that limit our ability, and the ability of certain of our subsidiaries, to: |

|||

• |

incur certain liens to secure indebtedness; |

|||

• |

engage in sale-leaseback transactions; and |

|||

• |

merge, amalgamate or consolidate or sell all or substantially all of such company's assets. |

|||

These covenants are subject to important exceptions and qualifications, which are described in "Description of the notes" under "— Covenants." See "Risk factors — Risks relating to the notes." |

||||

Exchange Offer and Registration Rights |

Under a registration rights agreement to be executed in connection with the offering of the notes, we will agree to: |

|||

• |

file a registration statement enabling holders to exchange the notes described in this offering memorandum for exchange notes that have been registered under the Securities Act; |

|||

• |

use our commercially reasonable efforts to consummate the exchange offer within 240 days after the issue date of the notes; and |

|||

6

• |

file a shelf registration statement for the resale of the notes offered hereby if we cannot effect the exchange offer within the time period referred to above, or under other circumstances specified in the registration rights agreement. |

|||

The interest rate on the notes will increase if we do not comply with certain of our obligations under the registration rights agreement. During the period we fail to comply with these obligations, we will pay additional interest on the notes at a rate of 0.50% per year for the first 90-day period following such failure, and a rate of 1.00% per year after the termination of such 90-day period following such failure, until the exchange offer is completed or the shelf registration statement, if required, is declared effective or the notes otherwise become freely tradable under the Securities Act. See "Exchange offer; Registration rights." |

||||

Transfer Restrictions |

The notes will be subject to certain restrictions on transfer. See "Transfer restrictions." |

|||

No Prior Market |

The notes will be new securities for which there is no market. Although the initial purchaser has informed us that it currently intends to make a market in the notes, it is not obligated to do so and may discontinue market-making at any time without notice. Accordingly, we cannot assure you that a liquid market will develop or be maintained. |

|||

Use of Proceeds |

We estimate that we will receive net proceeds of approximately $198.3 million from this offering, after deducting the initial purchaser's commissions and the estimated offering expenses. We intend to use the net proceeds from this offering to expand our retail network, invest in our manufacturing and logistics operations and for general corporate purposes. |

|||

7

Summary consolidated financial data

The following table sets forth selected consolidated financial data of Ethan Allen Interiors Inc. and its consolidated subsidiaries. The consolidated statements of operations data for the years ended June 30, 2003, 2004, and 2005, and the consolidated balance sheet data as of June 30, 2004 and 2005 have been derived from our consolidated financial statements, which have been audited by KPMG LLP, our independent auditors, and are incorporated by reference in this offering memorandum. The consolidated statements of operations data for the years ended June 30, 2001 and 2002, and the consolidated balance sheet data as of June 30, 2001, 2002 and 2003, are derived from our consolidated financial statements not included in this offering memorandum. Certain of the summary financial data for the year ended June 30, 2005, have been adjusted to reflect this offering and the initial application of the proceeds therefrom. You should read this data in conjunction with the "Selected financial data," and "Management's discussion and analysis of financial condition and results of operations" included in this offering memorandum.

| |

Fiscal Year Ended June 30, |

||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (Dollars in thousands, except per share data and financial ratios) |

|||||||||||||||||||||

| 2001 |

2002 |

2003 |

2004 |

2005 |

2005 |

||||||||||||||||

| |

|

|

|

|

|

(as adjusted) |

|||||||||||||||

| Statement of Operations Data: | |||||||||||||||||||||

| Net sales | $ | 904,133 | $ | 892,288 | $ | 907,264 | $ | 955,107 | $ | 949,012 | $ | 949,012 | |||||||||

| Cost of sales | 490,509 | 471,018 | 457,924 | 494,072 | 487,958 | 487,958 | |||||||||||||||

| Restructuring and impairment charge, net(1) | 6,906 | 5,123 | 13,131 | 12,520 | (219 | ) | (219 | ) | |||||||||||||

| Selling, general and administrative expenses | 281,723 | 286,888 | 316,752 | 322,111 | 332,295 | 332,295 | |||||||||||||||

| Operating income | 124,995 | 129,259 | 119,457 | 126,404 | 128,978 | 128,978 | |||||||||||||||

| Interest and other (income) expense, net | (2,056 | ) | (2,344 | ) | (517 | ) | (2,691 | ) | (442 | ) | (442 | ) | |||||||||

| Income before income tax expense | 127,051 | 131,603 | 119,974 | 129,095 | 129,420 | 129,420 | |||||||||||||||

| Income tax expense | 48,025 | 49,746 | 45,350 | 49,617 | 50,082 | 50,082 | |||||||||||||||

| Net income | 79,026 | 81,857 | 74,624 | 79,478 | 79,338 | 79,338 | |||||||||||||||

Balance sheet data (at end of period): |

|||||||||||||||||||||

| Cash and cash equivalents | $ | 48,112 | $ | 75,688 | $ | 54,356 | $ | 27,528 | $ | 3,448 | $ | 203,448 | |||||||||

| Total assets | 621,069 | 690,812 | 735,008 | 658,367 | 628,386 | 828,386 | |||||||||||||||

| Working capital | 183,863 | 193,354 | 228,177 | 161,772 | 130,423 | 330,423 | |||||||||||||||

| Current ratio | 2.70 | 2.50 | 2.70 | 2.18 | 1.97 | 3.47 | |||||||||||||||

| Total debt, including capital lease obligations | 9,487 | 9,321 | 10,218 | 9,221 | 12,510 | 212,510 | |||||||||||||||

| Shareholders' equity | 462,163 | 508,170 | 533,922 | 456,140 | 434,068 | 434,068 | |||||||||||||||

Other Financial Data: |

|||||||||||||||||||||

| Depreciation and amortization(2) | $ | 20,295 | $ | 19,503 | $ | 21,634 | $ | 21,854 | $ | 21,338 | $ | 21,338 | |||||||||

| Capital expenditures, including acquisitions(3) | 48,238 | 73,481 | 39,781 | 24,976 | 34,381 | 34,381 | |||||||||||||||

| Cash dividends declared(4) | 0.16 | 0.18 | 0.25 | 3.40 | 0.60 | 0.60 | |||||||||||||||

Other Operating Data: |

|||||||||||||||||||||

| EBITDA(5) | $ | 147,948 | $ | 151,606 | $ | 142,112 | $ | 151,449 | $ | 151,414 | $ | 151,414 | |||||||||

| Total debt to EBITDA | 0.06 | 0.06 | 0.07 | 0.06 | 0.08 | 1.40 | |||||||||||||||

| EBITDA to interest expense | 245.76 | 303.21 | 281.97 | 302.90 | 230.81 | 230.81 | |||||||||||||||

| Total number of stores owned | 312 | 316 | 309 | 311 | 313 | 313 | |||||||||||||||

| Number of company-owned stores | 84 | 103 | 119 | 127 | 126 | 126 | |||||||||||||||

| Number of independently-owned stores | 228 | 213 | 190 | 184 | 187 | 187 | |||||||||||||||

The footnotes to the preceding table appear on pages 19–20.

8

An investment in the notes involves a degree of risk. You should carefully consider the risks and uncertainties described below, in addition to the other information set forth in this offering memorandum, before purchasing the notes. The risks and uncertainties described below are not the only ones facing us. Additional risks and uncertainties not presently known to us or that we currently deem immaterial may also impair our financial condition, results of operations, cash flows or business. If any of the following risks or uncertainties actually occur, our financial condition, results of operations, cash flows or business could be materially or adversely affected.

We face changes in global and local economic conditions that may adversely affect consumer demand and spending, our manufacturing operations and sources of merchandise.

Historically, the home furnishings industry has been subject to cyclical variations in the general economy and to uncertainty regarding future economic prospects. We are currently confronted with the risk of increased expenses and decreased demand from customers as a result of Hurricane Katrina and other unfavorable weather conditions, natural disasters, the war in Iraq, armed conflicts and terrorist attacks. These global uncertainties, as well as other variations in global economic conditions such as rising fuel costs and increasing interest rates, may continue to cause inconsistent and unpredictable consumer spending habits, while increasing our own fuel, utility, transportation or security costs. These risks, as well as industrial accidents or work stoppages, could also severely disrupt our manufacturing operations, which could have a material adverse effect on our financial performance.

We import a portion of our merchandise from foreign countries. As a result, our costs may be increased by events affecting international commerce and businesses located abroad, including changes in international trade, central bank actions and other governmental policies of the U.S. and the countries from which we import a portion of our merchandise. The inability to import products from certain foreign countries or the imposition of significant tariffs could have a material adverse effect on our results of operations.

Competition from overseas manufacturers continues to increase and may adversely affect our business, operating results and financial condition.

Our wholesale business segment is involved in the development of our brand, which encompasses the design, manufacture, sourcing, sales and distribution of our home furnishings products, and competes with other U.S. and foreign manufacturers. Our retail business segment sells home furnishings to consumers through a network of company-owned stores, and competes against other retailers locally, regionally and nationally.

Our retail segment competes against a diverse group of retailers ranging from specialty stores to traditional furniture and department stores, and our competitors operate locally, regionally and nationally. We also compete with these and other retailers for appropriate retail locations as well as for qualified design consultants and management personnel. Such competition could adversely affect our future financial performance.

9

Industry globalization has led to increased competitive pressures brought about by the increasing volume of imported finished goods and components, particularly for case good products, and the development of manufacturing capabilities in other countries, specifically within Asia. The increase in overseas production capacity in recent years has created over-capacity for many U.S. manufacturers, including us, which has led to industry-wide plant consolidation. In addition, because many foreign manufacturers are able to maintain substantially lower production costs, including the cost of labor and overhead, imported product may be sold at a lower price to consumers which, in turn, has led to some measure of industry-wide price deflation.

We cannot assure you that we will be able to establish or maintain relationships with certain manufacturers, either abroad or domestically, to supply us with selected case goods, upholstery and home accessory items to enable us to maintain our competitive advantage. In addition, the recent emergence of foreign manufacturers has served to broaden the competitive landscape. Some of these competitors produce furniture types not manufactured by us and may have greater financial and other resources available to them. This competition could adversely affect our future financial performance.

Failure to successfully anticipate or respond to changes in consumer tastes and trends in a timely manner could adversely impact our business, operating results and financial condition.

Sales of our products are dependent upon consumer acceptance of our product designs, styles, quality and price. We continuously monitor consumer demand through internal marketing research and communication with our retailers and store design consultants who provide valuable input on consumer trends. As with all residential retailers, our business is susceptible to changes in consumer tastes and trends. Such tastes and trends can change rapidly and any delay or failure to anticipate or respond to changing consumer tastes and trends in a timely manner could adversely impact our business, operating results and financial condition.

Our success depends upon our brand, marketing and advertising efforts and pricing strategies, and if we are not able to maintain and enhance our brand or if we are not successful in these efforts, our business and operating results could be adversely affected.

Maintaining and enhancing our brand is critical to our ability to expand our base of customers and may require us to make substantial investments. Our advertising campaign uses television, direct mail, newspapers, magazines and radio to maintain and enhance our existing brand equity. We cannot assure you that our marketing, advertising and other efforts to promote and maintain our brand or our everyday best pricing strategy will not require us to incur substantial costs. If these efforts are unsuccessful or we incur substantial costs in connection with these efforts, our business, operating results and financial condition could be adversely affected.

Failure to protect our intellectual property could adversely affect us.

We believe that our patents, trademarks, service marks, trade secrets, copyrights and all of our other intellectual property are important to our success. We rely on patent, trademark, copyright and trade secret laws, and confidentiality and restricted use agreements, to protect our intellectual property and may seek licenses to intellectual property of others. Some of our intellectual property is not covered by any patent, trademark, or copyright or any applications for the same. We cannot assure you that agreements designed to protect our intellectual property will not be breached, that we will have adequate remedies for any such breach, or

10

that the efforts we take to protect our proprietary rights will be sufficient or effective. Any significant impairment of our intellectual property rights or failure to obtain licenses of intellectual property from third parties could harm our business or our ability to compete. Moreover, we cannot assure you that the use of our technology or proprietary know-how or information does not infringe the intellectual property rights of others. If we have to litigate to protect or defend any of our rights, such litigation could result in significant expense to us.

We may not be able to maintain our current store locations at current costs. We may also fail to successfully select and secure store locations.

Our stores are located in busy urban settings as freestanding destination stores or as part of suburban strip malls, depending upon the real estate opportunities in a particular market. Our business competes with other retailers and as a result, our success may be affected by our ability to renew current store leases and to select and secure appropriate retail locations for existing and future stores.

We depend on key personnel and could be affected by the loss of their services.

The success of our business depends upon the services of certain senior executives, and in particular, the services of M. Farooq Kathwari, Chairman of the Board, President and Chief Executive Officer, who is the only one of our senior executives who has a written employment agreement with us. The loss of any such person or other key personnel could have a material adverse effect on our business and results of operations.

Fluctuations in the price, availability and quality of raw materials could cause delay which could result in a decrease in our sales and increase costs, which could adversely impact our earnings.

We use various types of wood, fabrics, leathers, and other raw materials in manufacturing our furniture. Certain of our raw materials, including fabrics, are purchased both abroad and domestically. Fluctuations in the price, availability and quality of raw materials could cause increased costs or a delay, in manufacturing our products, which in turn could result in a delay in delivering products to our customers. For example, lumber prices fluctuate over time based on factors such as weather and demand, which in turn, impact availability. Upward trends in prices could have an adverse effect on margins. Delays or cost increases could lower our sales, adversely impacting our earnings.

In addition, certain suppliers may require extensive advance notice of our requirements in order to produce products in the quantities we desire. This long lead time may require us to place orders far in advance of the time when certain products will be offered for sale, thereby exposing us to risks relating to shifts in consumer demand and trends, and any downturn in the U.S. economy.

As we expand and grow our business, we may rely on external funding sources to finance our operations and growth.

Historically, we have relied upon our cash from operations to fund our operations and growth. As we expand our business, we may rely on external funding sources, which will include the proceeds from the issuance and sale of the notes and our $200 million revolving bank line of credit available under the credit facility. Any unexpected reduction in cash flow from operations could increase our external funding requirements to levels above those currently

11

available. There can be no assurance that we will not experience unexpected cash flow shortfalls in the future or that any increase in external funding required by such shortfalls will be available.

Our business is sensitive to increasing labor costs, competitive labor markets, our continued ability to retain high-quality personnel and risks of work stoppages.

The market for qualified employees and personnel in the retail and manufacturing industry is highly competitive. Our success depends upon our ability to attract, retain and motivate qualified craftsmen, management, marketing and sales personnel and upon the continued contributions of these individuals. We cannot assure you that we will be successful in attracting and retaining qualified personnel. A shortage of qualified personnel may require us to enhance our wage and benefits package in order to compete effectively in the hiring and retention of qualified employees. Our labor costs may continue to increase, and such increases may not be recovered. In addition, some of our employees are covered by collective bargaining agreements with local labor unions. Although we do not anticipate any difficulty renegotiating these contracts as they expire, a labor-related stoppage by these unionized employees could adversely affect our business and results of operations. The loss of the services of key personnel or our failure to attract additional qualified personnel could have a material adverse effect on our business, operating results and financial condition.

Our results of operations for any quarter are not necessarily indicative of our results of operations for a full year.

Sales of furniture and other home furnishing products fluctuate from quarter to quarter due to such factors as changes in global and regional economic conditions, changes in competitive conditions, changes in production schedules in response to seasonal changes in energy costs and weather conditions, and changes in consumer order patterns. From time to time, we have experienced, and may continue to experience, volatility with respect to demand for our home furnishing products. Accordingly, results of operations for any quarter are not necessarily indicative of the results of operations for a full year.

Our current and former manufacturing operations are subject to increasingly stringent health, safety and environmental requirements.

We use and generate hazardous substances in our manufacturing and retail operations. In addition, both the manufacturing properties on which we currently operate and those on which we have ceased operations are and have been used for industrial purposes. Our manufacturing operations and, to a lesser extent, our retail operations involve risks of personal injury or death. We are subject to increasingly stringent environmental, health and safety laws and regulations relating to our current and former properties and our current operations. These laws and regulations provide for substantial fines and criminal sanctions for violations and sometimes require the installation of costly pollution control or safety equipment or costly changes in operations to limit pollution or decrease the likelihood of injuries. In addition, we may become subject to potentially material liabilities for the investigation and cleanup of contaminated properties and to claims alleging personal injury or property damage resulting from exposure to or releases of hazardous substances or personal injury as a result of an unsafe workplace. We have been identified as a potential responsible party in connection with five sites that are currently listed, or proposed for inclusion, on the National Priorities List

12

under the Comprehensive Environmental Response, Compensation and Liability Act or its state counterpart. In addition, noncompliance with, or stricter enforcement of, existing laws and regulations, adoption of more stringent new laws and regulations, discovery of previously unknown contamination or imposition of new or increased requirements could require us to incur costs or become the basis of new or increased liabilities that could be material.

We are subject to restrictive covenants and conditions under our credit facility. We are also subject to certain covenants and conditions under the indenture. These covenants and conditions could significantly affect the way in which we conduct our business and restrict our ability to repay the notes. Our failure to comply with these covenants could lead to an acceleration of our debt.

The credit facility contains a number of covenants that, among other things, restrict our ability to dispose of assets, incur additional indebtedness, repay or refinance other indebtedness or amend other debt instruments, create liens on assets, make investments or acquisitions, engage in mergers or consolidations, and make certain payments and investments. The credit facility also requires us to comply with specified financial covenants, including a fixed charge coverage ratio and a maximum leverage ratio. The indenture contains covenants that limit our ability to incur certain liens to secure indebtedness, engage in sale-leaseback transactions or merge, amalgamate, consolidate or sell all or substantially all of our assets.

Our ability to continue to comply with these covenants and conditions may be affected by events beyond our control. The breach of any of the covenants contained in the credit facility or failure to comply with certain conditions, including the continued accuracy of our representations and warranties, unless waived by the lenders, would be a default under the credit facility. This would permit the lenders to accelerate the maturity of the credit facility. It would also permit the lenders to terminate their commitments to extend credit under the credit facility. This could have an immediate material adverse effect on our liquidity. An acceleration of maturity of the credit facility may permit the holders of the notes to accelerate the maturity of the notes. Acceleration of maturity of the notes would permit the lenders to accelerate the maturity of the credit facility and terminate their commitments to extend credit under our revolving credit facility, unless we were able to obtain a waiver from the lenders. We cannot assure you that we would have sufficient funds to make these accelerated payments or that we would be able to obtain any such waiver on acceptable terms or at all.

Our ability to service our debt, including the notes, and meet our other obligations depends on certain factors beyond our control.

Our ability to service our debt, including the notes, and meet our other obligations as they come due is dependent on our future financial and operating performance. This performance is subject to various factors, including certain factors beyond our control such as, among other things, changes in global and regional economic conditions, changes in consumer demand for, and acceptance of, our products, changes in our industry, changes in interest rates and inflation in raw materials, energy and other costs.

If our cash flow and capital resources are insufficient to enable us to service our debt and meet these obligations as they become due, we could be forced to reduce or delay capital

13

expenditures, sell assets or businesses, limit or discontinue, temporarily or permanently, business plans, activities or operations, obtain additional debt or equity financing, or restructure or refinance debt. We cannot assure you as to the timing of such actions or the amount of proceeds that could be realized from such actions.

The notes will be structurally subordinated to creditors of our subsidiaries that are not guarantors of the notes.

Ethan Allen Interiors Inc., one of the guarantors, is the parent company. It is a holding company with no material operations or assets other than the common stock of Ethan Allen Global. Its principal liabilities consist of its guarantees of the credit facility and the notes, and guarantees of debt and commercial obligations of Ethan Allen Global's subsidiaries. Although Ethan Allen Global is the issuer, a substantial majority of our assets, on a consolidated basis, are held by Ethan Allen Retail, Inc., Ethan Allen Operations, Inc., Ethan Allen Realty, LLC and other subsidiary guarantors. In addition, some of our assets are held by subsidiaries that are not guarantors. Our ability, and the ability of noteholders, to realize upon the assets of any subsidiary that is not a guarantor of the notes in any liquidation, bankruptcy, reorganization or similar proceedings involving such subsidiary will be subject to the claims of their respective creditors, including their respective trade creditors and holders of their respective debt. As a result, the notes will be structurally subordinated to all existing and future debt and other obligations, including trade payables, of our subsidiaries that are not guarantors of the notes. At June 30, 2005, on an as adjusted basis after giving effect to the sale of the notes and the application of the proceeds therefrom, the debt and liabilities of such non-guarantor subsidiaries would have totaled approximately $8.6 million (excluding intercompany trade and other miscellaneous liabilities of approximately $10.8 million).

Except as otherwise noted in this risk factor, the financial information included or incorporated by reference in this offering memorandum is presented on a consolidated basis. As a result, such financial information does not completely indicate the historical or as adjusted assets, liabilities or operations of each source of funds for payment of debt service on the notes.

Because the notes are not secured, future secured lenders will have a prior claim on our secured assets.

The notes and our current credit facility are not secured by any of our assets. While the indenture does have limitations on liens that we can incur to secure indebtedness, we may incur some secured indebtedness in the future without securing the notes. Therefore, if we become insolvent or are liquidated, or if payment under the notes is accelerated, the lenders under such instruments would be entitled to exercise the remedies available to secured lenders under applicable law and pursuant to instruments governing such indebtedness. Accordingly, such lenders will have a prior claim on those of our assets securing their indebtedness. Because the notes are not secured by any of our assets, it is possible that there would be no assets remaining from which claims of the holders of the notes could be satisfied or (if any such assets remained) such assets might be insufficient to satisfy such claims in full.

14

In the event of the bankruptcy or insolvency of Ethan Allen Interiors Inc. or any of the subsidiary guarantors, the guarantee of the notes by Ethan Allen Interiors Inc. or such subsidiary could be voided and subordinated.

In the event of the bankruptcy or insolvency of Ethan Allen Interiors Inc. or any of the subsidiary guarantors, its guarantee would be subject to review under relevant fraudulent conveyance, fraudulent transfer, equitable subordination and similar statutes and doctrines in a bankruptcy or insolvency proceeding or a lawsuit by or on behalf of creditors of that guarantor. Under those statutes and doctrines, if a court were to find that the guarantee was incurred with the intent of hindering, delaying or defrauding creditors or that the guarantor received less than a reasonably equivalent value or fair consideration for its guarantee and, at the time of its incurrence, the guarantor:

then the court could void or subordinate its guarantee. If the guarantee of a guarantor is voided or subordinated, holders of the notes would effectively be subordinated to all indebtedness and other liabilities of that guarantor.

We cannot assure you that an active trading market will develop for the notes.

The notes will be a new issue of securities for which there is currently no public trading market. We are selling the notes under exemptions from registration under applicable securities laws. Therefore, the notes may not be publicly offered, sold or otherwise transferred in any jurisdiction where such registration may be required. As a result, there will be no public trading market for the notes.

The initial purchaser has informed us that it intends to make a market in the notes. The initial purchaser is, however, not obligated to make a market in the notes, and it may discontinue any market-making activities with respect to the notes at any time without notice. Any such market-making activity may be limited during the pendency of an exchange offer or the effectiveness of an exchange offer registration statement, or under certain circumstances, a shelf registration statement, pursuant to the registration rights agreement.

The liquidity of the trading market in the notes, and the market price quoted for the notes, may be adversely affected to a material degree by, among other things, changes in:

As a result, we cannot assure you that an active trading market will develop or, if developed, will continue for the notes. If a market does develop, the price of the notes may fluctuate and

15

liquidity may be limited. If a market for the notes does not develop, you may be unable to resell the notes for an extended period of time, if at all.

The notes are subject to restrictions on transfer.

The notes have not been registered under the Securities Act or any state or foreign securities laws. Absent registration, the notes may be offered or sold only in transactions that are not subject to, or that are exempt from, the registration requirements of the Securities Act and applicable state or foreign securities laws. Although we have agreed to use our best efforts to file, and to have declared effective, a registration statement under the Securities Act relating to an exchange offer for the notes, we cannot assure you that such a registration statement will become or remain effective.

The SEC has broad discretion to determine whether any registration statement will be declared effective and may delay or deny the effectiveness of any registration statement for a variety of reasons. Failure to have such a registration statement declared effective could adversely affect the liquidity and price of the notes.

16

We estimate that the net proceeds to us from this offering (after deducting the initial purchaser's discount and estimated fees and expenses of this offering) will be approximately $198.3 million. We intend to use the net proceeds to us from this offering to expand our retail network, invest in our manufacturing and logistics operations and for general corporate purposes.

Pending use for a specific purpose, we may initially use a portion of the net proceeds to reduce the outstanding balance under the credit facility, if any, and, to the extent that at the time there is no such amount outstanding, to invest in investment quality, interest-bearing securities or deposits with maturities not to exceed 24 months. The credit facility matures in 2010. The credit facility bears interest at a variable rate equal to the greatest of the Prime Rate of JPMorgan Chase Bank, N.A., the Federal Funds Rate plus .5%, or a third composite of interest rates plus 1%, plus additional fees whose percentages are tied to our credit ratings as issued by Moody's and Standard and Poor's. At June 30, 2005, the outstanding balance under our credit facility was $8.0 million.

J.P. Morgan Securities Inc. or its affiliates are lenders under the credit facility and will receive their proportionate shares of any repayment of amounts under the credit facility as described above.

17

The following table sets forth our capitalization as of June 30, 2005 (i) on an actual basis and (ii) as adjusted to reflect this offering and the initial application of the estimated net proceeds therefrom. You should read this table in conjunction with "Use of proceeds," "Selected financial data" and "Management's discussion and analysis of financial condition and results of operations" included, and the consolidated financial statements and the notes thereto incorporated by reference, in this offering memorandum.

| |

June 30, 2005 |

|||||||

|---|---|---|---|---|---|---|---|---|

| (Dollars in thousands) |

Actual |

As Adjusted |

||||||

| Cash and cash equivalents | $ | 3,448 | $ | 203,448 | ||||

| Short-term debt | 240 | 240 | ||||||

| Long-term debt | $ | 12,270 | 212,270 | |||||

| Shareholders' equity | ||||||||

| Class A common stock, par value $.01, 150,000,000 shares authorized, 46,585,896 shares issued at June 30, 2005 | 466 | 466 | ||||||

| Class B common stock, par value $.01, 600,000 shares authorized; no shares issued and outstanding at June 30, 2005 | — | — | ||||||

| Preferred stock, par value $.01, 1,055,000 shares authorized, no shares issued and outstanding at June 30, 2005 | — | — | ||||||

| Additional paid-in capital | 302,620 | 302,620 | ||||||

| 303,086 | 303,086 | |||||||

| Less: | ||||||||

| Treasury stock (at cost), 12,071,866 shares at June 30, 2005 | (337,635 | ) | (337,635 | ) | ||||

| Retained earnings | 467,566 | 467,566 | ||||||

| Accumulated other comprehensive income | 1,051 | 1,051 | ||||||

| Total shareholders' equity | 434,068 | 434,068 | ||||||

| Total capitalization(1) | $ | 446,338 | $ | 646,338 | ||||

(1) As of August 31, 2005, our total capitalization was approximately $421.1 million, consisting of the sum of our long-term debt and total shareholders' equity of $13.8 million and $407.3 million, respectively.

18

The following table sets forth selected consolidated financial data of Ethan Allen Interiors Inc. and its consolidated subsidiaries. The consolidated statements of operations data for the years ended June 30, 2003, 2004, and 2005, and the consolidated balance sheet data as of June 30, 2004 and 2005 have been derived from our consolidated financial statements, which have been audited by KPMG LLP, our independent auditors, and are incorporated by reference in this offering memorandum. The consolidated statements of operations data for the years ended June 30, 2001 and 2002, and the consolidated balance sheet data as of June 30, 2001, 2002 and 2003, are derived from our consolidated financial statements not included in this offering memorandum. Certain of the summary financial data for the year ended June 30, 2005, have been adjusted to reflect this offering and the initial application of the proceeds therefrom. You should read the information below in conjunction with "Management's discussion and analysis of financial condition and results of operations" included in this offering memorandum.

| |

Fiscal Year Ended June 30, |

||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (Dollars in thousands, except per share data and financial ratios) |

2001 |

2002 |

2003 |

2004 |

2005 |

2005 (as adjusted) |

|||||||||||||||

| Statement of Operations Data: | |||||||||||||||||||||

| Net sales | $ | 904,133 | $ | 892,288 | $ | 907,264 | $ | 955,107 | $ | 949,012 | $ | 949,012 | |||||||||

| Cost of sales | 490,509 | 471,018 | 457,924 | 494,072 | 487,958 | 487,958 | |||||||||||||||

| Restructuring and impairment charge, net(1) | 6,906 | 5,123 | 13,131 | 12,520 | (219 | ) | (219 | ) | |||||||||||||

| Selling, general and administrative expenses | 281,723 | 286,888 | 316,752 | 322,111 | 332,295 | 332,295 | |||||||||||||||

| Operating income | 124,995 | 129,259 | 119,457 | 126,404 | 128,978 | 128,978 | |||||||||||||||

| Interest and other (income) expense, net | (2,056 | ) | (2,344 | ) | (517 | ) | (2,691 | ) | (442 | ) | (442 | ) | |||||||||

| Income before income tax expense | 127,051 | 131,603 | 119,974 | 129,095 | 129,420 | 129,420 | |||||||||||||||

| Income tax expense | 48,025 | 49,746 | 45,350 | 49,617 | 50,082 | 50,082 | |||||||||||||||

| Net income | 79,026 | 81,857 | 74,624 | 79,478 | 79,338 | 79,338 | |||||||||||||||

| Balance sheet data (at end of period): | |||||||||||||||||||||

| Cash and cash equivalents | $ | 48,112 | $ | 75,688 | $ | 54,356 | $ | 27,528 | $ | 3,448 | $ | 203,448 | |||||||||

| Total assets | 621,069 | 690,812 | 735,008 | 658,367 | 628,386 | 828,386 | |||||||||||||||

| Working capital | 183,863 | 193,354 | 228,177 | 161,772 | 130,423 | 330,423 | |||||||||||||||

| Current ratio | 2.70 | 2.50 | 2.70 | 2.18 | 1.97 | 3.47 | |||||||||||||||

| Total debt, including capital lease obligations | 9,487 | 9,321 | 10,218 | 9,221 | 12,510 | 212,510 | |||||||||||||||

| Shareholders' equity | 462,163 | 508,170 | 533,922 | 456,140 | 434,068 | 434,068 | |||||||||||||||

| Other Financial Data: | |||||||||||||||||||||

| Depreciation and amortization(2) | $ | 20,295 | $ | 19,503 | $ | 21,634 | $ | 21,854 | $ | 21,338 | $ | 21,338 | |||||||||

| Capital expenditures, including acquisitions(3) | 48,238 | 73,481 | 39,781 | 24,976 | 34,381 | 34,381 | |||||||||||||||

| Cash dividends declared(4) | 0.16 | 0.18 | 0.25 | 3.40 | 0.60 | 0.60 | |||||||||||||||

| Other Operating Data: | |||||||||||||||||||||

| EBITDA(5) | $ | 147,948 | $ | 151,606 | $ | 142,112 | $ | 151,449 | $ | 151,414 | $ | 151,414 | |||||||||

| Total debt to EBITDA | 0.06 | 0.06 | 0.07 | 0.06 | 0.08 | 1.40 | |||||||||||||||

| EBITDA to interest expense | 245.76 | 303.21 | 281.97 | 302.90 | 230.81 | 230.81 | |||||||||||||||

| Total number of stores owned | 312 | 316 | 309 | 311 | 313 | 313 | |||||||||||||||

| Number of company-owned stores | 84 | 103 | 119 | 127 | 126 | 126 | |||||||||||||||

| Number of independently-owned stores | 228 | 213 | 190 | 184 | 187 | 187 | |||||||||||||||

| Ratio of earnings to fixed charges(6) | 17.82 | 16.79 | 13.35 | 13.14 | 12.43 | 12.43 | |||||||||||||||

(1) In the fourth quarter of fiscal 2004, we announced a plan to close and consolidate two of our manufacturing facilities. The plants, both involved in the production of case goods, were located in Boonville, New York and Bridgewater, Virginia. The plant closures resulted in a headcount reduction totaling approximately 460 employees: 270 employees effective June 25, 2004 and 190 employees throughout the first quarter of fiscal 2005. A pre-tax restructuring and impairment charge of $12.8 million was recorded for costs associated with these plant closings, of which $4.5 million related to employee severance and benefits and other plant exit costs, and $8.3 million related to fixed asset impairment charges, primarily for real property and machinery and equipment associated with the closed facilities. During the first six months of fiscal 2005, the final cash payments relating to these plant closings were made and certain adjustments totaling $0.2 million were recorded to reverse the remaining previously established accruals which were no longer required.

In the third quarter of fiscal 2003, we announced a plan to close three of our smaller manufacturing facilities. Closure of these facilities resulted in a headcount reduction totaling approximately 580 employees: 340 employees effective

19

April 21, 2003 and 240 employees throughout the last quarter of fiscal 2003 and the first quarter of fiscal 2004. A pre-tax restructuring and impairment charge of $13.4 million was recorded for costs associated with these plant closings, of which $4.5 million related to employee severance and benefits and other plant exit costs, and $8.9 million related to fixed asset impairment charges, primarily for real property and machinery and equipment associated with the closed facilities. During the first quarter of fiscal 2004, adjustments totaling $0.2 million were recorded to reverse certain of these previously established accruals which were no longer required.

In the fourth quarter of fiscal 2002, we announced a plan that involved the closure of one of our manufacturing facilities as well as the rough mill operation of a separate facility. Closure of these facilities resulted in a headcount reduction totaling approximately 220 employees: 150 employees effective June 29, 2002 and 70 employees throughout the first quarter of fiscal 2003. A pre-tax restructuring and impairment charge of $5.1 million was recorded for costs associated with these plant closings, of which $2.0 million related to employee severance and benefits and other plant exit costs, and $3.1 million related to fixed asset impairment charges, primarily for real property and machinery and equipment associated with the closed facilities. During the third quarter of fiscal 2003, adjustments totaling $0.2 million were recorded to reverse certain of these previously established accruals which were no longer required.

In the fourth quarter of fiscal 2001, we announced a plan that involved the closure of three of our manufacturing facilities and a headcount reduction totaling approximately 350 employees effective August 6, 2001. A pre-tax restructuring and impairment charge of $6.9 million was recorded for costs associated with these plant closings, of which $3.3 million related to employee severance and benefits and other plant exit costs, and $3.6 million related to fixed asset impairment charges, primarily for real property and machinery and equipment associated with the closed facilities. During the first quarter of fiscal 2002, adjustments totaling $0.1 million were recorded to reverse certain of these previously established accruals which were no longer required.

(2) As a result of our adoption of Statement of Financial Accounting Standards ("SFAS") No. 142, Goodwill and Other Intangible Assets, amortization of goodwill and indefinite-lived intangible assets ceased on July 1, 2001. The amount of amortization related to these assets totaled $1.8 million in fiscal 2001.

(3) Capital expenditures are principally attributable to (i) new store development and renovation, (ii) company-wide technology initiatives and (iii) improvements within our manufacturing and logistics operations. Acquisitions include the purchase of 1 retail store and 1 manufacturing facility in 2001, 20 retail stores in 2002, 16 retail stores in 2003, 4 retail stores in 2004, and 6 retail stores in 2005.

(4) On April 27, 2004, we declared a special, one-time cash dividend of $3.00 per common share, payable on May 27, 2004 to shareholders of record as of May 10, 2004.

(5) EBITDA, for this purpose, means net income, plus interest expense, income tax expense, depreciation and amortization. We believe that EBITDA is an important indicator of our operational strength and performance of our business, including our ability to pay interest, service debt and fund capital expenditures. Given the nature of our operations, including the tangible assets necessary to carry out our production and distribution activities, depreciation and amortization represent our largest non-cash charges. As these non-cash charges do not affect our ability to service debt or make capital expenditures, it is important to consider EBITDA in addition to, but not as a substitute for, operating income, net income and other measures of financial performance reported in accordance with generally accepted accounting principles ("GAAP"), including cash flow measures such as operating cash flow. Further, EBITDA is one measure used to determine compliance with our existing credit facility. Our method for calculating EBITDA may not be comparable to methods used by other companies. The following table sets forth, for the periods indicated, the calculation of EBITDA, presenting a reconciliation to the GAAP measure of net income:

| |

Year Ended June 30, |

|||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| (Dollars in millions) |

2001 |

2002 |

2003 |

2004 |

2005 |

2005 (as adjusted) |

||||||||||||

| Net income | $ | 79,026 | $ | 81,857 | $ | 74,624 | $ | 79,478 | $ | 79,338 | $ | 79,338 | ||||||

| Plus: Interest expense | 602 | 500 | 504 | 500 | 656 | 656 | ||||||||||||

| Plus: Income tax expense | 48,025 | 49,746 | 45,350 | 49,617 | 50,082 | 50,082 | ||||||||||||

| Plus: Depreciation and amortization | 20,295 | 19,503 | 21,634 | 21,854 | 21,338 | 21,338 | ||||||||||||

| EBITDA | $ | 147,948 | $ | 151,606 | $ | 142,112 | $ | 151,449 | $ | 151,414 | $ | 151,414 | ||||||

(6) For purposes of determining the ratio of earnings to fixed charges, "earnings" is the amount resulting from (i) adding the following items: (a) pretax income from continuing operations before adjustment for minority interests in consolidated subsidiaries or income or loss from equity investees, (b) fixed charges, and (c) amortization of capitalized interest, and (ii) subtracting interest capitalized. "Fixed charges" means the sum of the following: (a) interest expensed and capitalized, (b) amortized premiums, discounts and capitalized expenses related to indebtedness, and (c) an estimate of the interest within rental expense.

20

Management's discussion and analysis of financial condition and results of operations

The following discussion of financial condition and results of operations is based upon, and should be read in conjunction with, the consolidated financial statements and notes thereto incorporated by reference in this offering memorandum.

Critical accounting policies

Our consolidated financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America which require, in some cases, that certain estimates and assumptions be made that affect the amounts and disclosures reported in those financial statements and the related accompanying notes. Estimates are based on currently known facts and circumstances, prior experience and other assumptions believed to be reasonable. Management uses its best judgment in valuing these estimates and may, as warranted, solicit external advice. Actual results could differ from these estimates, assumptions and judgments, and these differences could be material. The following critical accounting policies, some of which are impacted significantly by estimates, assumptions and judgments, affect our consolidated financial statements.