EXHIBIT 1

SANDELL SENDS LETTER TO CHAIRMAN AND CEO OF ETHAN ALLEN INTERIORS INC.

Sees Value of $41 per Share in either Recapitalization or Sale, Over 30% Above Current Price

Sandell Prepared to Nominate Slate of Directors for October 15 Annual Meeting

Prospective Purchasers of Ethan Allen Shares Encouraged to Pursue Settlement of Purchases on a “T+1” Basis; Sandell Believes August 17 is Record Date for Upcoming Annual Meeting

New York (August 14, 2015) - Sandell Asset Management Corp. (“Sandell”), the beneficial owner of approximately 1.6 million shares, or 5.5%, of Ethan Allen Interiors Inc. (“Ethan Allen” or the “Company”) (NYSE:ETH), today sent a letter to Farooq Kathwari, the Chairman and CEO of Ethan Allen.

In the letter, Sandell notes its belief that the Company’s stock is trading at a significant discount to its intrinsic value, which Sandell believes is approximately $41 per share, or over 30% above where the stock is currently trading. Sandell believes that a combination of sub-optimal fiscal policies and inefficient allocation of shareholder capital has contributed to the significant discount in the shares, as Ethan Allen has underperformed its publicly-traded peers by 119% over the last 10 years. Sandell believes that the Company’s extensive portfolio of real estate assets may be worth approximately $450 million, or about $16 per share, and that the Company has the ability to greatly enhance shareholder value through either a recapitalization and a monetization of its real estate holdings, or through a sale to a private equity firm. Sandell believes that either path would result in a value of at least $41 per share delivered to shareholders.

Ethan Allen on August 12 responded to Sandell’s overtures to the Company by manipulating the corporate franchise and advancing the date of its 2015 Annual Meeting of Shareholders (the “Annual Meeting”) to October 15, more than one month in advance of the previously expected November 17 date as set forth in the Company’s last proxy statement. This new advanced date was “publicly announced” by the Company on page 19 of its recently-filed 10-K. Sandell is

prepared to nominate a slate of Director candidates to stand for election at the Company’s 2015 Annual Meeting, although it hopes to re-engage with the Company to reach an amicable resolution and avoid a proxy contest.

Sandell believes that August 17 is the record date for the upcoming Annual Meeting, and reminds shareholders that any shares held in margin accounts that may be loaned by a broker will need to be moved into a cash account in advance of the record date if shareholders want to vote their shares. Also, any prospective purchasers of Ethan Allen shares prior to August 17 are encouraged to pursue settlement of purchases on a “T+1” basis if shareholders want to vote such shares.

The text of the letter is as follows:

August 14, 2015

Mr. Farooq Kathwari

Chairman, CEO and President

Ethan Allen Interiors Inc.

Ethan Allen Drive

Danbury, CT 06811

Dear Farooq:

As you know, we are significant shareholders of Ethan Allen Interiors Inc. (“Ethan Allen” or the “Company”) and currently own approximately 1.6 million shares, or 5.5%, of the Company. We appreciate the dialogue that my colleague Richard Mansouri and I have had with you and the Company’s CFO Corey Whitely over the last few months. It should be clear to you that our firm strongly believes in the significant value associated with the assets that constitute Ethan Allen, not least of which is the Company’s iconic brand name, which connotes home furnishings of un-paralleled quality. Unfortunately, what should also be clear to you is that the Company’s stock price is significantly below Ethan Allen’s true intrinsic value, which we believe is approximately $41 per share, or over 30% higher than its current price.

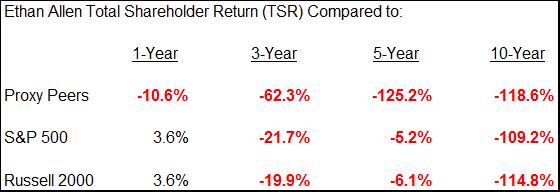

It is also unfortunate that, while you have led Ethan Allen for close to 30 years and have built a unique business of substance, shareholders have suffered extended and material underperformance due in large part to what we believe to be the Company’s sub-optimal fiscal policies and inefficient allocation of shareholder capital over the last several years. Indeed, Ethan Allen serves as an abject example of the ill effects that can befall shareholders invested in a company that does not earn an appropriate return on its capital. The following chart shows in stark detail the underperformance that shareholders have been subjected to:

Source: Bloomberg (as of 7/8/15, the day prior to media reports of private equity interest). Proxy peers include BSET,HVT,HNI,KNL,LZB,MLHR,PIR,RL,SCS,SCSS,TPX,TIF,WSM.

As you can see, Ethan Allen has underperformed its peers over each time period, with 10-year underperformance versus its peers a staggering 119%. Moreover, Ethan Allen’s current stock price is actually below where it was in August of 2005, indicating that shareholders have witnessed negative absolute price performance over 10 years in addition to suffering a wide gap in relative performance. Perhaps because of this staggering underperformance, the Company chose to take what we believe was the outrageous step of advancing the date of its 2015 Annual Meeting. Specifically, we find buried in the Company’s recently-filed 10-K that Ethan Allen intends to hold its 2015 Annual Meeting of Shareholders (the “Annual Meeting”) on October 15, more than one month in advance of the previously expected November 17 date as set forth in the Company’s last proxy statement. We have little doubt that the Company was seeking to catch shareholders unaware, as the nomination window for submitting shareholder proposals and nominations for directors is tied to the date of its Annual Meeting.

Clearly, the capital tied up in the Company’s vast portfolio of real estate assets has been a drag on shareholder returns. You in fact provide damning commentary when you stated in a press release dated April 14, 2015: “Since going public, the company has invested in capital expenditures of $747.9 million including investments in retail and manufacturing properties and acquisitions.” We note that the market value of Ethan Allen today is not meaningfully higher than the aggregate $747.9 million that you have expended over the last 22 years since going public in 1993. Had the Company earned an appropriate rate of return on this invested capital over the years, the market value of the Company would be far greater than what it is today. Sadly, the Company has still shown no indication that it intends to tap into the exceedingly robust market for both retail and industrial real estate properties in order to unlock this capital that has been trapped on its balance sheet.

We believe that Ethan’s Allen’s sizable stable of properties, which includes: 53 wholly-owned retail design centers; 17 retail design centers subject to ground leases; its corporate

headquarters building and 18.0 acre campus; its 200 room Hotel and Conference Center; and its eight wholly-owned manufacturing facilities, as well as various ancillary properties, is worth approximately $450 million, or about $16 per share, little of which we believe is reflected in Ethan Allen’s current stock price. To put this in perspective, the value of the Company’s real estate is over 50% of Ethan Allen’s entire market value. Furthermore, we believe based upon input from numerous finance and real estate experts that there are many interested parties and several ways to help the Company unlock this value, ranging from a series of sale-leaseback transactions to the creation of a tax-efficient REIT through an OpCo-PropCo structure.

Along with the trapped capital associated with the Company’s extensive real estate holdings is the Company’s highly-inefficient balance sheet. As of June 30, 2015, Ethan Allen actually had negative net debt. That the Company continues to operate with net leverage below zero while Ethan Allen’s stock trades at a price below where it was 10 years ago reflects an astonishingly unsophisticated fiscal policy that we believe is at odds with the fundamental precepts of modern corporate finance, a policy which is even more troubling when one considers that prevailing interest rates remain close to historical lows. And while we have no doubt you will seek to trumpet the Company’s history of returning capital to shareholders (“Since going public” appears to be your favored yardstick for measuring Company history, even though that spans a period of 22 years), recent action by Ethan Allen paints an entirely different picture. To illustrate, we note that in Fiscal 2012 the Company purchased a mere 79,000 shares, or less than 0.3% of total shares outstanding, and in Fiscal 2013 and 2014, the Company did not repurchase any shares at all. Only very, very recently did the Company step up its repurchase activity (542,000 shares repurchased in 4Q Fiscal 2015) and only after a dramatic fall in stock price following Ethan Allen’s 3Q Fiscal 2015 earnings disappointment.

We are not suggesting that you alone are responsible for what we believe to be the Company’s misguided fiscal policies and underperformance; the entire Board of Directors must shoulder this blame. In this regard, we note that while you are the longest-standing Director, having been appointed to the Board 27 years ago, there are three other Directors who have been on the Board for more than 10 years, namely: Frank Wisner (14 years); Kristin Gamble (23 years) and Clinton Clark (26 years). So many long-tenured directors can lead to a dangerous level of complacency which we believe has been manifest at Ethan Allen.

Fortunately, the Company has within its control the ability to take steps to greatly enhance shareholder value. There are multiple alternatives available to the Company, though they can be generalized as two discrete paths that we believe Ethan Allen should consider, namely: (1) a recapitalization and monetization of its extensive real estate holdings and (2) a sale to a private equity firm. We believe it is imperative that the Company announce the retention of an impartial, nationally-recognized investment banking firm as soon as possible in order to aid the Company in the exploration of these alternatives.

The first path would contemplate a recapitalization through the incurrence of a reasonable amount of debt (Net Debt equal to 2.5x Pro-Forma EBITDA) coupled with the tax-efficient monetization of the Company’s real estate holdings, possibly by way of an OpCo-PropCo structure. In such a scenario, Ethan Allen could repurchase a meaningful number of shares, possibly by way of a Dutch tender, and subsequently issue by way of a special dividend additional cash and/or shares of a real estate PropCo. Were the Company to pursue such a tax-efficient recapitalization, we believe shareholders could receive total consideration of at least $41 per share. As a show of good faith, we would be prepared to sign an agreement seeking to maintain our existing percentage equity ownership (at minimum) pro-forma for the repurchase of shares in a Dutch tender, as we firmly believe that the pursuit of such a recapitalization would lead to the creation of significant future equity value and we would like to maintain a meaningful equity investment in the Company.

Should Ethan Allen instead seek to pursue a sale to a private equity firm, we have no doubt that there would be a “line out the door” of interested parties seeking to acquire the Company. Indeed, we are aware of multiple private equity professionals who have expressed interest in pursuing an acquisition of Ethan Allen. The unique characteristics of the Company, such as Ethan Allen’s exceptional brand name recognition, its robust free cash flow, its minimal core capital spending requirements, and its unlevered balance sheet and extensive real estate holdings make Ethan Allen an ideal, and in fact almost prototypical, LBO candidate.

What is perhaps most compelling is the fact that you are intimately familiar with the process of consummating an acquisition of Ethan Allen. As we have discussed with you on multiple occasions, you were directly responsible for spearheading the LBO of Ethan Allen in 1989 when a consortium led by management took the Company private. Today’s environment is much, much more hospitable to financing acquisitions than it was in 1989. We note that Ethan Allen had to pay an interest rate of 18.17% before refinancing bonds associated with the Company’s acquisition in 1989 whereas today we believe a private equity sponsor could easily procure bank financing at an interest rate in the vicinity of 4% to 5%. We believe that a purchase of Ethan Allen at $38 per share should generate an IRR of 20% annually to a private equity sponsor, which is a remarkably attractive return profile, while a purchase at $41 per share should still generate an IRR greater than 15% annually, a benchmark threshold for many sponsors.

As a final note, please understand that unlike many chief executives of publicly-traded companies that we have encountered, we hold you in higher regard for the meaningful amount of stock that you personally own. It is our hope that we can engage in immediate dialogue in order to devise a solution that will result in a dramatic enhancement of shareholder value. Notwithstanding the Company’s apparent under-handed attempt to subvert the nomination process by advancing the date of the 2015 Annual Meeting, we are prepared to nominate a slate of Director candidates to stand for election at the Company’s 2015 Annual Meeting,

though we hope that it will not be necessary to engage in a contentious proxy battle in order to achieve the goal of enhanced shareholder value that we could easily accomplish by working together.

Sincerely,

Thomas E. Sandell

Chief Executive Officer

cc: The Board of Directors

About Sandell Asset Management Corp.

Sandell Asset Management Corp. is a leading private, alternative asset management firm specializing in global corporate event-driven, multi-strategy investing with a strong focus on equity special situations and credit opportunities. Sandell Asset Management Corp. was founded in 1998 by Thomas E. Sandell and has offices in New York and London, including a global staff of investment professionals, traders and infrastructure specialists.

Contact:

Sandell Asset Management Corp.

Adam Hoffman, 212-603-5814

Okapi Partners LLC

Bruce Goldfarb, 212-297-0722 or Chuck Garske, 212-297-0724

Sloane & Company

Elliot Sloane, 212-446-1860 or Dan Zacchei, 212-446-1882

SANDELL ASSET MANAGEMENT CORP., CASTLERIGG MASTER INVESTMENTS LTD., CASTLERIGG INTERNATIONAL LIMITED, CASTLERIGG INTERNATIONAL HOLDINGS LIMITED, CASTLERIGG OFFSHORE HOLDINGS, LTD., CASTLERIGG ACTIVE INVESTMENT FUND, LTD., CASTLERIGG ACTIVE INVESTMENT INTERMEDIATE FUND, L.P., CASTLERIGG ACTIVE INVESTMENT MASTER FUND, LTD., CASTLERIGG EQUITY EVENT AND ARBITRAGE FUND, PULTENEY STREET PARTNERS, L.P., THOMAS E.

SANDELL (COLLECTIVELY, THE “PARTICIPANTS”), INTEND TO FILE WITH THE SECURITIES AND EXCHANGE COMMISSION (THE “SEC”) A DEFINITIVE PROXY STATEMENT AND ACCOMPANYING FORM OF PROXY CARD TO BE USED IN CONNECTION WITH THE SOLICITATION OF PROXIES FROM THE STOCKHOLDERS OF ETHAN ALLEN INTERIORS INC. (THE “COMPANY”) IN CONNECTION WITH THE COMPANY’S 2015 ANNUAL MEETING OF STOCKHOLDERS. ALL STOCKHOLDERS OF THE COMPANY ARE ADVISED TO READ THE DEFINITIVE PROXY STATEMENT AND OTHER DOCUMENTS RELATED TO THE SOLICITATION OF PROXIES BY THE PARTICIPANTS WHEN THEY BECOME AVAILABLE, AS THEY WILL CONTAIN IMPORTANT INFORMATION, INCLUDING ADDITIONAL INFORMATION RELATED TO THE PARTICIPANTS. WHEN COMPLETED, THE DEFINITIVE PROXY STATEMENT AND AN ACCOMPANYING PROXY CARD WILL BE FURNISHED TO SOME OR ALL OF THE COMPANY’S STOCKHOLDERS AND WILL BE, ALONG WITH OTHER RELEVANT DOCUMENTS, AVAILABLE AT NO CHARGE ON THE SEC’S WEBSITE AT HTTP://WWW.SEC.GOV/.

INFORMATION ABOUT THE PARTICIPANTS AND A DESCRIPTION OF THEIR DIRECT OR INDIRECT INTERESTS BY SECURITY HOLDINGS WILL BE CONTAINED IN AN EXHIBIT TO THE SCHEDULE 14A TO BE FILED BY SANDELL ASSET MANAGEMENT CORP. WITH THE SEC ON AUGUST 14, 2015. THIS DOCUMENT CAN BE OBTAINED FREE OF CHARGE FROM THE SOURCES INDICATED ABOVE.